Business Description

Taiwan Semiconductor Manufacturing Company (TSM) is the world's leading dedicated semiconductor foundry, playing a crucial role in the global technology landscape. Unlike Integrated Device Manufacturers (IDMs) like Intel, which design and manufacture their own chips, TSM focuses solely on manufacturing chips designed by its customers. This "fabless" model allows companies like Apple, AMD, and Nvidia to focus on chip design and innovation without the massive capital expenditure and complexity of building and operating advanced fabrication facilities (fabs).

(by Amit Hattangadi)

Its focus on fabless has been working very well thanks to specialization that allows TSM to take orders from big customers like Apple and Nvidia. The large volume of orders allow TSM to pour large amount of money in R&D for the cutting edge chips manufacturing:

(from Yole Group)

For integrated circuits (chip) manufacturing, TSM has a market share of over 60%. For advanced chips (7nm or under), TSM has a market share of over 90%. Those chips are used to power the cutting edge technology in our world, like Smartphones, AI training and inferencing (for their related applications: chatbots, machine-learning powered algorithms, Self-driving vehicles, etc.), cloud, etc.

Today, TSM is a driving force in technological advancement, playing a crucial role in shaping the future. In my opinion, its success come down to:

The right execution strategy (fabless, and willing to spend lot in R&D)

Government support (Taiwan)

Having a talented pool at relatively low cost (Taiwan)

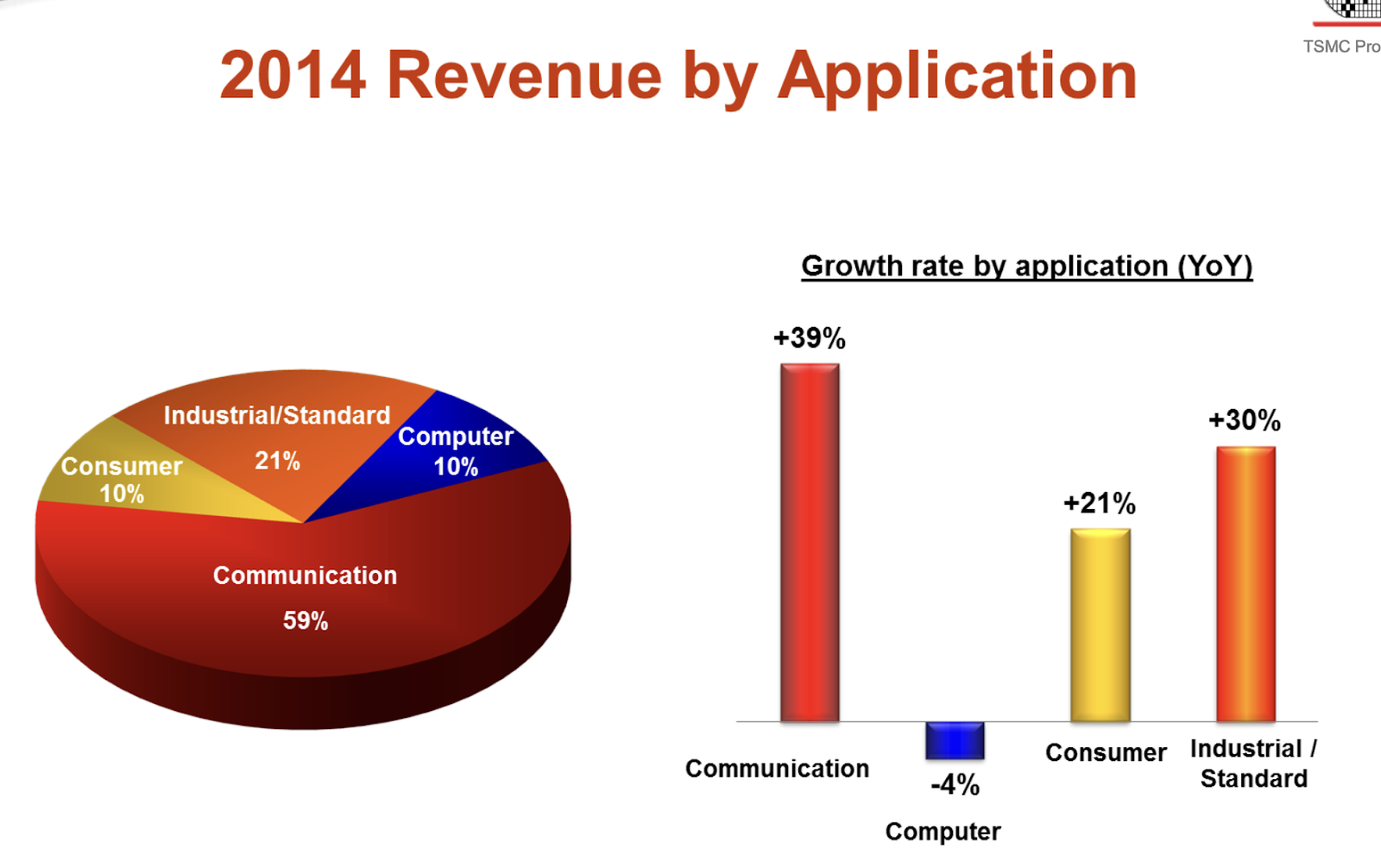

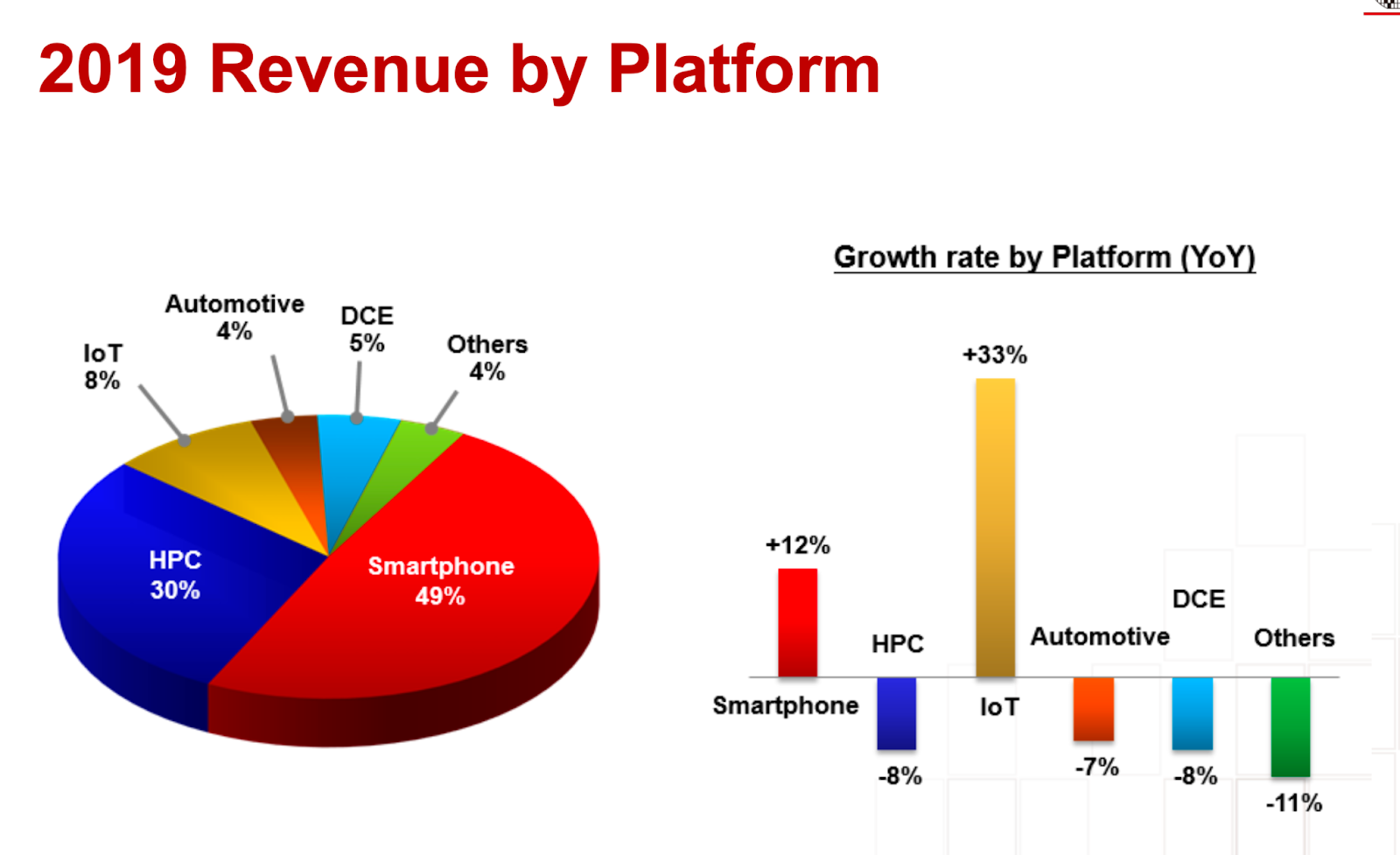

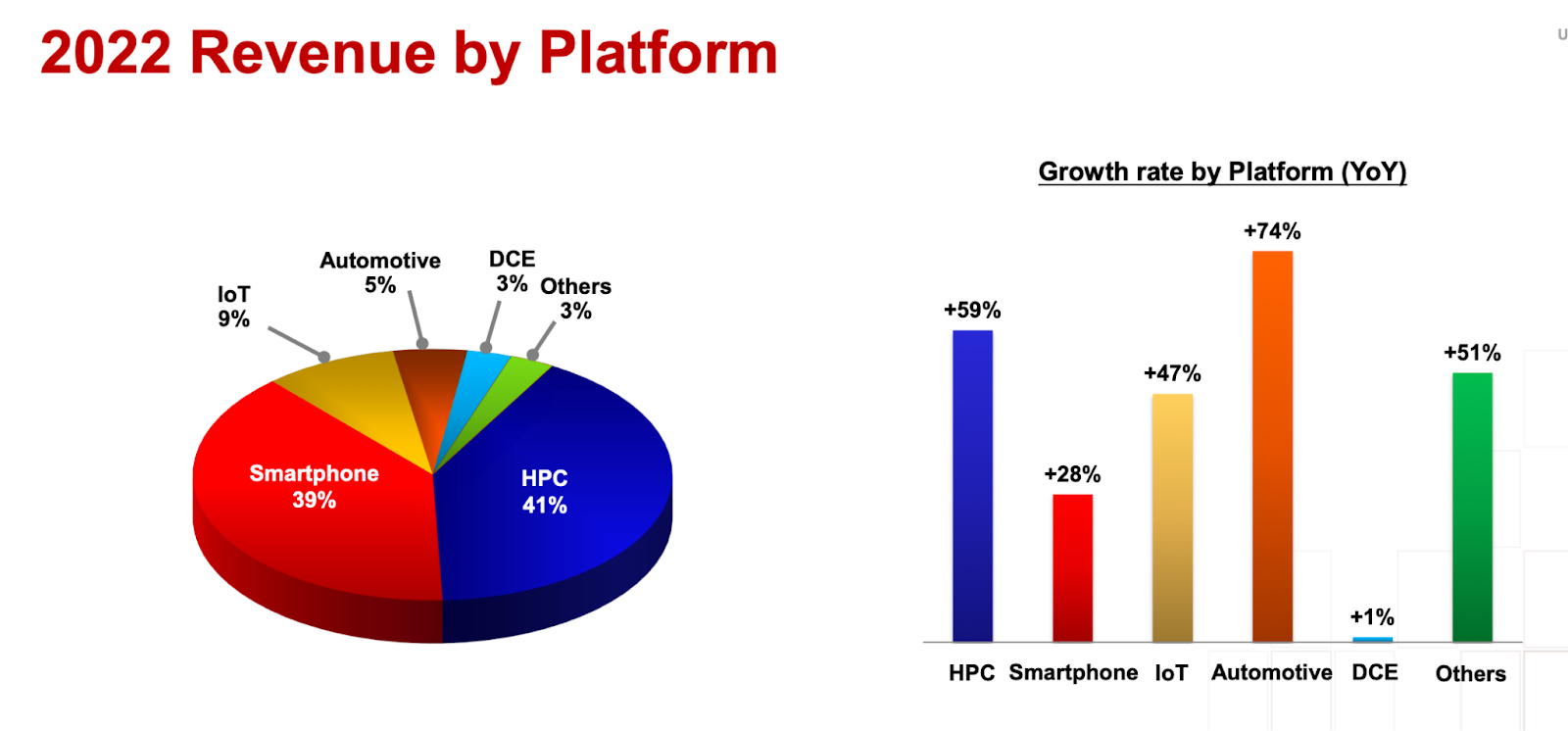

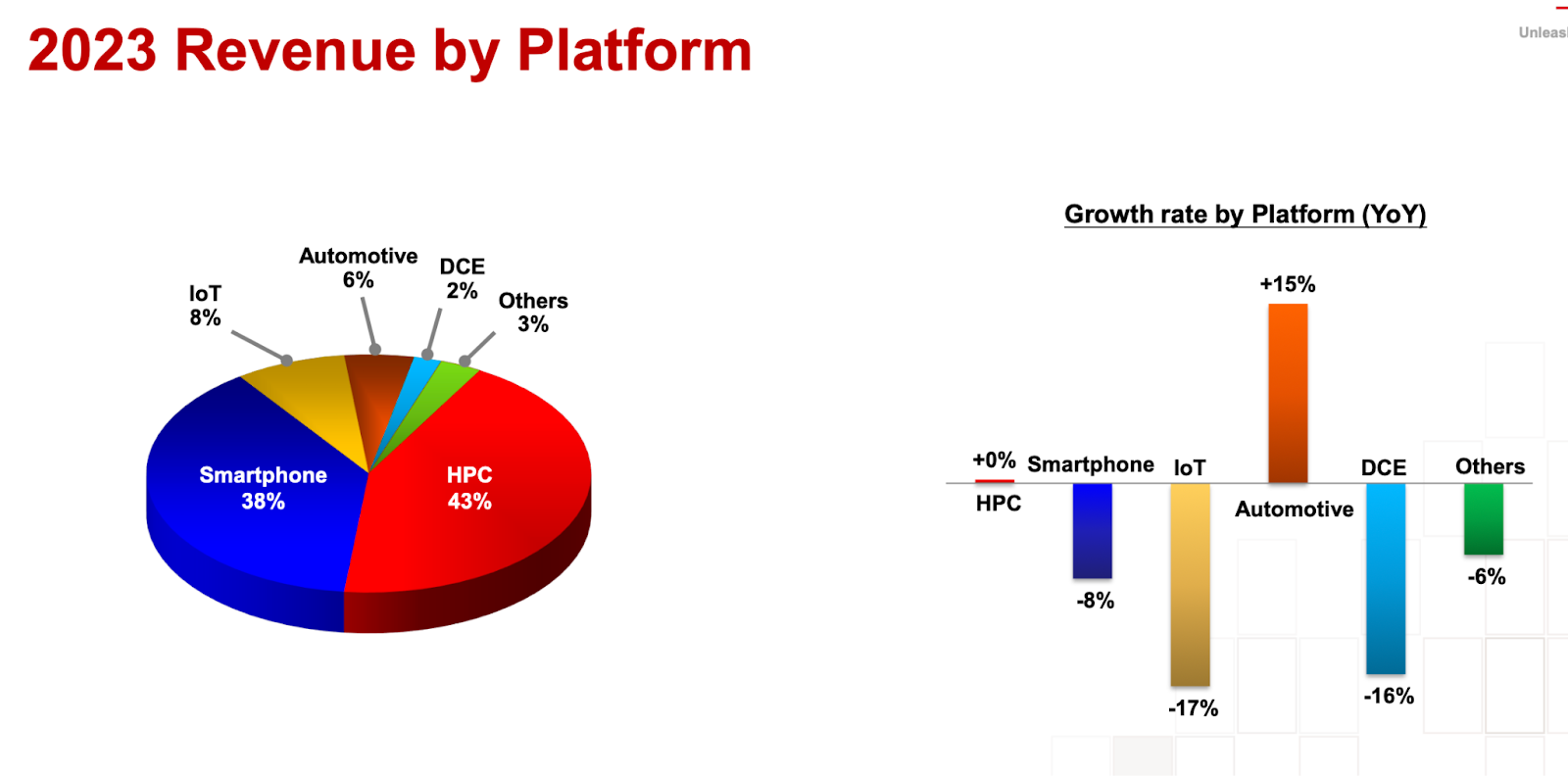

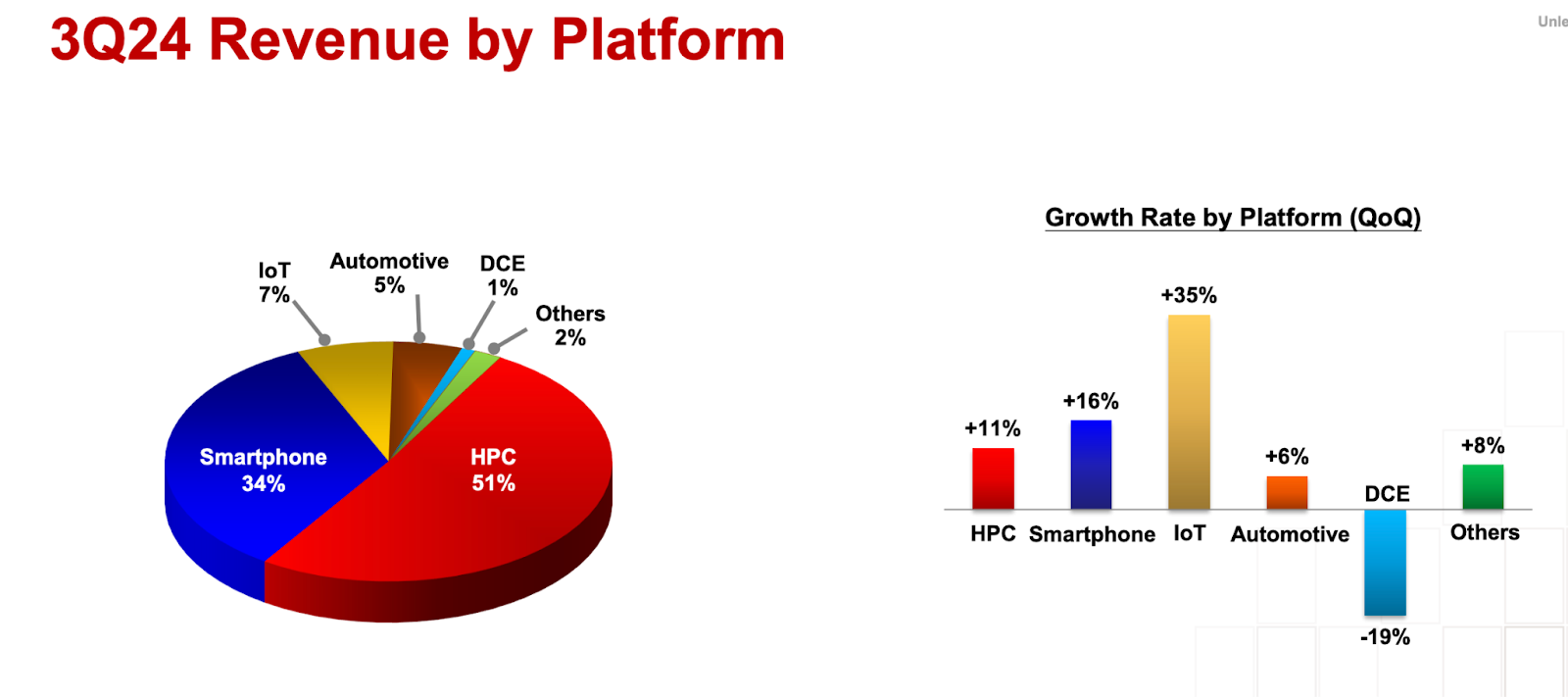

As of 2024, TSM's end markets include:

High-Performance Computing (HPC) (~50%): This segment is experiencing rapid growth due to the rise of artificial intelligence, data centers, and cloud computing. Companies like Nvidia, AMD and Google are major customers in this space. The increasing adoption of AI and the growth of data-intensive applications are expected to drive strong growth in this segment.

Smartphone & Tablet (~35%): This segment is driven by the continuous demand for high-performance, energy-efficient chips in mobile devices. Apple is TSM's largest customer. This segment is expected to maintain steady growth, fueled by increasing smartphone penetration in emerging markets and the continuous demand for more powerful mobile devices.

Internet of Things (IoT) (7%): As more devices become interconnected, the demand for specialized, low-power chips to power IoT applications is increasing. This segment encompasses a wide range of applications, from smart home devices to industrial sensors, and is expected to experience significant growth in the coming years.

Automotive (5%): The automotive industry is undergoing a significant transformation with the rise of electric vehicles and autonomous driving, leading to increased demand for advanced chips for applications like infotainment, power management, and ADAS (Advanced Driver-Assistance Systems). This segment is poised for rapid growth as the automotive industry continues to electrify and automate.

Digital consumer electronics and others(3%): This segment encompasses various applications like consumer electronics, industrial equipment, and digital consumer electronics.

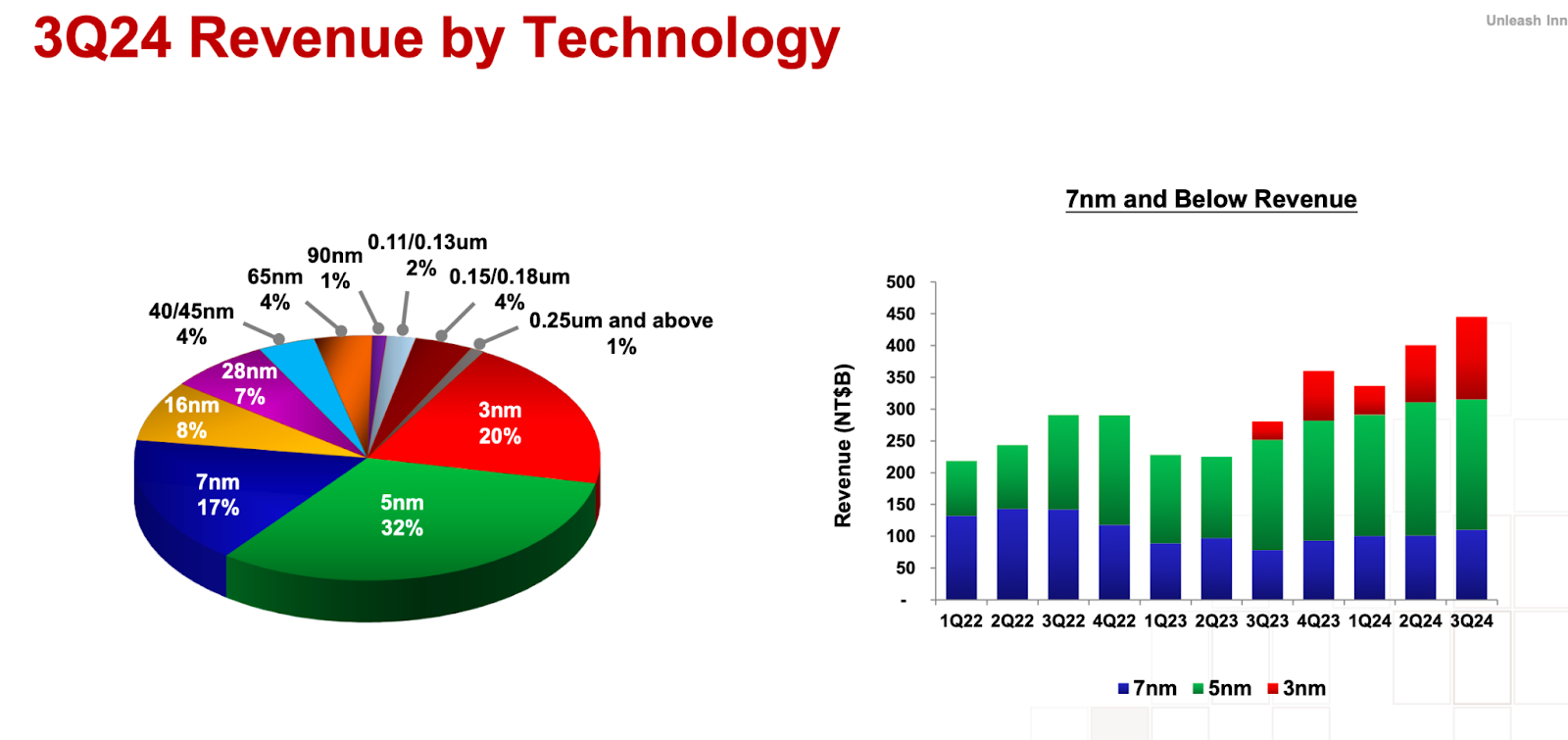

Technology wise, 7nm and below has the largest pie of the revenue, and TSM is a clear market leader on this segment:

In the year of 2023, TSM has:

SWOT analysis

Strengths

TSM enjoys significant cost advantages due to its massive scale, efficient operations, and learning curve advantages. These cost advantages allow TSM to offer competitive pricing while maintaining high margins, making it difficult for competitors to undercut them.

The semiconductor foundry industry has extremely high barriers to entry. Building advanced fabs requires tens of billions of dollars in capital investment, cutting-edge technology, access to scarce resources like EUV lithography machines, and specialized expertise. Catching up to TSM's technological lead is a daunting task, deterring new entrants.

TSM has a concentrated customer base, with its top 10 customers accounting for a significant portion of its revenue. This gives large customers like Apple some negotiating leverage. However, TSM's technological leadership, limited alternative foundry options for advanced chips, and the critical role it plays in its customers' product roadmaps provide counterbalance.

TSM's technological leadership is its primary competitive advantage. The company consistently invests heavily in R&D, enabling it to maintain its position at the forefront of semiconductor manufacturing technology. This allows TSM to produce the most advanced chips, which command premium pricing and attract leading fabless companies. That in turn allows TSM to pour more money in R&D to maintain its edge. It's a nice flywheel there.

Based in Taiwan and being the most important company in Taiwan, it has tremendous government support, and it's beloved by the people. A strong infrastructure was built in Taiwan to make semiconductor manufacturing easy. Also, Taiwan has a highly educated population while the living standard is not high compared to other developed countries, which provides TSM a good source of talent with relatively low cost.

Weaknesses

While TSM has advantage in its higher yield in production (less defects), its products are commodities that can be manufactured by Samsung and Intel (albeit with higher costs due to lower yield).

Customers have relatively low switching cost and tend to source chips from more than just TSM.

Semiconductor manufacturing is resource-intensive and has environmental implications. Taiwan is not an energy rich country, so TSM may face limitations in energy for its manufacturing.

Chips demand was cyclical in the historical context, so there can be a downturn in the industry and there is not much TSM can do about it. Its huge capex may make it suffer losses in the downturn of the cycle.

Opportunities

Developed countries like the United States know the importance of chips manufacturing, so they provide lucrative incentives for TSM to build factories there. It helps TSM to diversify its source of manufacturing.

The AI boom lit by the LLM is real. There will be lots of applications and lots of demand for advanced chips.

Threats

The biggest threat for TSM is the geopolitical risk due to the China-Taiwan relationship. Threats from China to Taiwan can seriously disrupt the supply for TSM, and make its customers lose confidence in the company.

Intel and Samsung are catching up. They are also willing to pour huge R&D do their foundry businesses with the backing of national support. For Intel, it treats the foundry business as determining its life or death, and it is exploring new technology which may overtake TSM. Intel will be the first semiconductor foundry to use backside power delivery in a process node, which can increase power efficiency and reduce interference in chips. TSM has a lot to lose if losing the number one spot in chip manufacturing. It always has to keep improving to be ahead of everyone else.

There maybe a plateau in chips manufacturing that even the manufacturing process becomes a commodity that eliminates TSM's edge.

Alternative computing architectures like quantum computing are being explored, they are still in early stages of development and may pose threat to TSM's core business in the future.

References

TSM quarterly reports from official website: https://investor.tsmc.com/english/quarterly-results/2024/q3

2024/07/25 Chip king TSMC, where will it go after a trillion-dollar market value?

2024/05/24 TSMC: The Most Mission-Critical Company on Earth

Updates

2024/10/28 Valuation

EPS estimate is $7.05 in 2024 and $8.79 in 2025 (from Seeking Alpha)

The analysts are expecting about 15% annual revenue growth for the next 5 years. I am a bit more optimistic because the AI boom lit by various LLM models is real and AI will play a much larger role in people's lives. There will be more demand for advanced chips in smartphones, vehicles, Internet of things, etc. Thus, I am assuming 20% annual earnings growth for 10 years.

Assuming a terminal P/E of 20, and a 15% discount rate, the buy below price is:

$7.05 * (1+20%)^10 * 20 / (1+15%)^10 ~ $215. That is a 2024 P/E of 30.5x

A caveat is that TSM's free cash flow seems to be only about half of its earnings, so there is some downside risk in valuation.

Given the geopolitical risk due to the China-Taiwan relationships, I would limit TSM's position to at most 10% of the portfolio.

2024/10/24 The Future of Taiwan and the Investment Decision on TSM

Blog post published and copied verbatim below:

On 2023/02/17, I said that I would follow Warren Buffett to avoid the geopolitical risk of Taiwan. The endgame, or the "ultimate resolution" between Taiwan and China is very uncertain that will likely involve economic disruptions, so I would avoid buying more Taiwan Semiconductor Manufacturing Company (TSM). That made me missing the boat as shown in the chart below that, the price more than doubled since then (from $90 to ~$200):

[a chart that shows the price of TSM at about $198]

While the company is solid, I want to revisit the geopolitical risk of Taiwan to see whether I should jump back into TSM. After reading a lot of opinions from various experts, I got the following conclusion with the help of Gemini:

Most experts believe that the status quo is likely to persist for the next decade or more. This is based on the current balance of power, the lack of political will on either side for a drastic change, and the potential costs and risks associated with any attempt to alter the status quo.

Does it mean I will likely resume my purchase of TSM? Yes, but it will be at most 10% of my portfolio, and likely less.

What do I think about the current valuation of TSM? I think it's fairly valued, so it's acceptable to buy more at the current price given the company has a very strong moat. More analysis soon!

2023/02/17

Gave up hope in TSM given Buffett sold it (news). While the company is solid, it has some political risk. Buffett's sale is a signal that I might have underestimated the risk. By the principle of this portfolio, I am not selling the existing stake.

2022/05/31 brief assessment

Taiwan Semiconductor is a global leader in chip manufacturing. It has passed Intel and is getting farther and farther ahead of Intel. It has a wide economic moat as a popular company in Taiwan beloved by common people. It's a national treasure.

With all technological gadgets today requiring chips to operate, including military weapons, its business is neverending. Supply problems are just small hiccups which do not hurt the fundamentals of the company.

2022 P/E is less than 20. It has a dividend yield of 2%, and growing 10-20% every year, not bad at all.

No comments:

Post a Comment