Business Description

Patria is a leading Latin American private markets investment firm with 30+ years of history. They boast combined assets under management (AUM) of $28.4 billion (of which $21.4 billion are fee-earning) and a global presence with offices in 10 cities across 4 continents. Patria acts as a gateway for Latin American and global capital to invest in Latin American alternative investments; and for Latin American capital to invest in global alternative investments.

Through a diversified platform spanning Private Equity, Infrastructure, Credit, Public Equities and Real Estate strategies, Patria provides a comprehensive range of products to serve its global client base.

Patria has a long-term track record of outperformance:

AUM in percentages under each segment by the end of 2023 Q3:

Patria did quite a lot of acquisitions lately. And by the end of December, 2023, Patria was expected to have $33 billion AUM after all the transactions were closed. The breakdown is:

The strategic pillars of growth are:

increase product offering

expand geographic footprint

extend client base

strengthen the platform

All these are aimed to create a strong and resilient business model anchored on long-term AUM and predictable Fee Related Earnings.

In 2023 Q3, Patria earned $61.6 million total fee revenues, $36 million fee-related earnings (58% margin). Distributable earnings of $34.6 million, which is $0.23 per share. Shares outstanding: 147,875,671.

YTD, Patria earned $179.6 million total fee revenues and $101 million fee-related earnings (56% margin).

Patria has no debt.

Its 2025 target shows the expectation of at least 15% growth in fee related earnings:

SWOT analysis

Strengths

Good track record on performance:

private equities and infrastructure has overall IRR of 15+% in BRL, 12+% return in USD

public equities: 240 to 520 basis points of excess return

credit: 90 to 190 basis points of excess return

real estate/agribusiness: this is a downer, negative 10% in BRL

in-house sector knowledge to capitalize on powerful secular trends in the region

"boots on the ground" in target markets

Partnerships with Blackstone: The company was 40% owned by Blackstone at some point, and was now reduced to 14%. This investment provides Patria with access to Blackstone's global network and resources, which has helped them to grow their business significantly. Patria is often referred to as the "mini-Blackstone" of Latin America. This is due to its similarities to Blackstone in terms of business model, investment strategy, and track record.

Weaknesses

Only 20% of the asset under management is in permanent capital, so the fee-related earnings can be unstable.

Not as scalable and well reputed as other big dogs like Blackstone, Brookfield, KKR. However, the partnership with Blackstone helped a lot to mitigate this scale issue.

Country concentration risk: Latin America economy may not be as promising as it looks.

Short tenure as a public company. It was IPO'ed in 2021.

Opportunities

As of 2023 Q3, the company had no debt and had over $200 million in short-term investments. This is a lot of dry powder to do M&A to consolidate the industry.

Small enough to have a long runway to grow in the industry. Being a leader in Latin America, it definitely has potential to be the Blackstone of Latin America.

The global trend of institutions to pivot capital to private equity.

Threats

Reputation risk: performance can be unstable

References

December 2023 Shareholder Presentation

Third party articles:

2022/12/21: My Largest HYI Investment For 2023 by High Yield Landlord

2022/02/02: My Largest LatAm Investment Right Now by High Yield Landlord

Updates

2024/12/14 Update valuation after Patria 2024 Investor Day Presentation

2024/12/09 Patria 2024 Investor Day Presentation

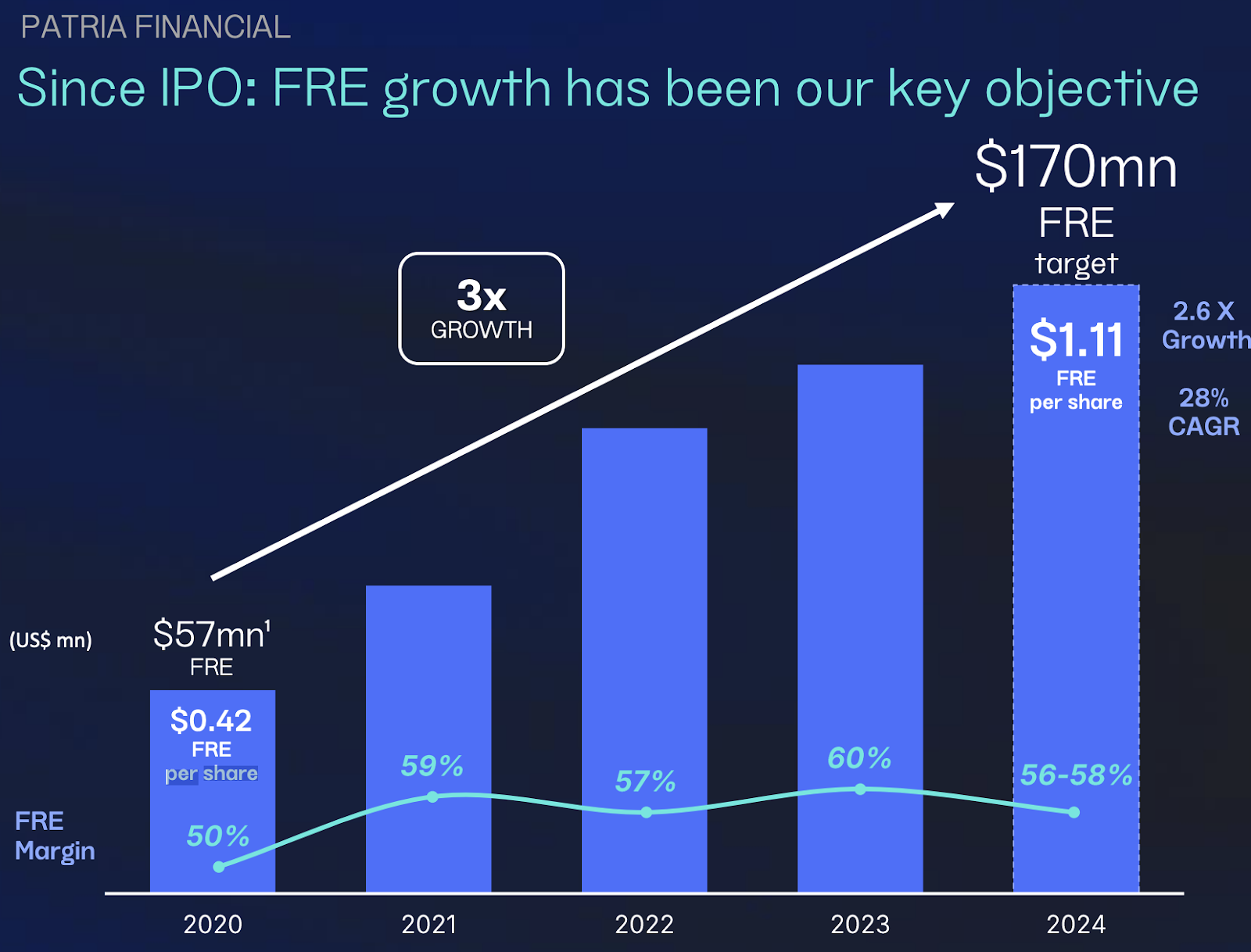

PAX has been growing rapidly at absolute level and also at per-share level on the key metric: Fee-related earnings (FRE):

And it's going to grow 15% annually to at least 2027:

That means PAX is expected to earn $1.7 FRE per share in 2027 at mid-point guidance:

If we assume distributed earnings (DE) is 90% of that, and adjusted DE is 70% of DE due to shared-based compensation, it will earn $1.7 * 0.9 * 0.7 = $1.07 adjusted DE per share in 2027.

Using a 20x multiple, the valuation will be at $1.07 * 20 = $21.4. Using a discount rate (required return) of 15% to discount it back two years to get the current valuation (buy below price), we get $21.4/(1.15^2) = $16.18. That is, even if we buy it at $16.18 today, we can earn 15% annually in share price appreciation plus about 3.7% dividend yield. And the current share price is $12.7, which is at a 21% discount of my buy below price, so it is very attractive today.

2024/08/16 2024 Q2 earnings update and brief valuation

TRADE ALERT - International Portfolio July 2024 (New Investment) and a follow-up after earnings TRADE ALERT - Core & International Portfolio August 2024 by High Yield Landlord gave me a lot more confidence with the company. Two quotes from the 2024 Q2 earnings call are worth mentioning:

Our confidence in our business outlook is further demonstrated by the fact that Patria Holding Limited, or PHL, the controlling shareholder of Patria Investments Limited and the vehicle through which senior management of Patria stake is held, is committing to purchase up to an additional $12.5 million of PAX shares through the end of 2025 on top of the share repurchase program. As a reminder, PHL currently owns a majority stake of more than 53% in Patria. These actions, in addition to our intention to utilize up to $100 million of future PRE to fund M&A and/or pay down M&A related debt and now to potentially repurchase stock as well demonstrates that we will be flexible and opportunistic as we look to use our capital to drive profitable FRE and DE growth and long-term returns to shareholders while optimizing and maintaining a conservative balance sheet, which is of the highest priority and which Ana will review in more detail shortly. So even with the change of our dividend at the current stock price, the current yield is a solid of about 5%.

We expect FRE per share to rise to $1.10 and $1.12 for 2024 from our previous guidance of $1.09, which reflects our expectation that the 2024 year-end share count will be modestly lower than we had previously guided to as we issue fewer shares and we use more cash to fund M&A and related contingencies. Our 2025 FRE per share guidance comes in at $1.26 to $1.41 with a midpoint of $1.34. At midpoint, this represents a 20% year-over-year growth.We expected a strong FRE growth to also drive accelerated DE per share growth into 2025 as we move past from loaded M&A financing costs and excluding the DE impact of any performance fees. Overall, we are even more excited about the growth opportunity that lies ahead.

The management expects the FRE to grow 20% next year, which is very great given the P/ADE (my adjusted distributable earnings) is just 16.79x. It has a dividend yield of about 5%, and I expect it to grow its earnings per share around 12% annually. It is trading at such a great bargain for such a promising company that no wonder High Yield Landlord touted it as an investment with a "combination of high yield, upside, growth, and safety." PAX's management also has so much confidence in the company that they are committing to purchase more shares in PAX. In addition, PAX will also start repurchasing its shares. I will keep buying more heavily if the share price stays this low.

I started with a conservative distributable earnings estimation of $1 for 2024, then reducing 30% of it due to non-cash compensation. I believe the company is worth a 20 multiple of that adjusted distribution earnings due to the high dividend payout and a sustainable 12-15% annual earnings growth.

Below use the management's guidance of $1.34 per share of Fee-related earnings in 2025, and my estimate of dividend based on 85% of distributable income.

2024/07/02 brief valuation

2024/02/23 Update with 2023 Q4 earnings result

The Q4 earnings were great with $1.26 distributable earnings for the whole year of 2023. AUM grew 17%. Revenue from services and distributable income both went up more than 20%. The company is firing on all cylinders, and the management guided for 20% annual growth for at least two more years.

For valuation, I would take a 30% cut on distributable earnings because they excluded stock-based compensation, etc. Using that number with a 20 multiple, the buy below price is $1.26 * 0.7 * 20 = $17.64. It is quite cheap at the current price of $15.

2023/12/12 Valuation

The 2023 Q3 number was recent and was quite clean, so I used it as a baseline. Distributable earnings was $34.6 million. I deducted $1.6 million net financial income due to it being uncertain and it can be positive or negative depending on the cash position. I also deducted $1.1 million long term employee benefits due it being a real expense. That gave me $31.9 million. That is $0.21 per share (total shares outstanding: 147,875,671), annualized to $0.84. It's capable of growing annually at 10 to 15+%, so it's worth at least P/DE = 20x = $16.8 per share.

It pays a variable dividend because Patria aims to pay about 85% of its distributable earnings in dividends. The upcoming dividend is estimated to be at least $0.8 a share. At the current price of $14.3, that is a5.5% dividend yield.

No comments:

Post a Comment