Business Description

Brookfield Corporation (BN) is a leading global investment firm with a long history of delivering strong returns for shareholders. The company has three core businesses:

Alternative Asset Management: Brookfield manages a diverse portfolio of assets, including renewable power, infrastructure, private equity, real estate, and credit. The company earns asset management income by managing investments for institutional and retail clients

Wealth Solutions: Brookfield offers a range of wealth management solutions, including retirement services, institutional investments, and private market solutions.

Operating Businesses: Brookfield owns and operates businesses in renewable power, infrastructure, business and industrial services, and real estate.

Brookfield has a track record of delivering 15%+ annualized returns to shareholders for over 30 years. The company's success is attributed to its proven investment and operational expertise and its global reach.

SWOT analysis

Strengths

Brand Reputation: Brookfield has a strong track record of generating attractive returns for investors over the long term. This has built significant trust and confidence among institutional investors.

Scale: Brookfield's large scale provides significant advantages. It can access larger and more complex deals, negotiate favorable terms with sellers and lenders, and spread its costs across a large AUM base.

Operational Expertise: Brookfield has a deep bench of experienced professionals with expertise in managing and optimizing the performance of its diverse assets. Its ability to run the business it invests in is a differentiation that allows Brookfield to enhance its investment return.

Global Reach: Brookfield has a global presence, with offices and investments in various markets around the world. This allows it to capitalize on investment opportunities across different geographies and diversify its portfolio. This global footprint also allows Brookfield to gather various local data to aid its investment decision.

Superior capital allocation: by repurchasing shares opportunistically, Brookfield is able to enhance return for shareholders. The strong alignment of interest by the management helps a lot here.

Weaknesses

Exposure to Economic Cycles: The performance of its investments can be affected by economic downturns and market volatility.

Reliance on Debt Financing: Brookfield uses significant leverage to finance its investments, which can amplify risks during economic downturns.

Opportunities

De-carbonization, de-globalization (onshore infrastructure opportunities), and digitalization provides plenty of opportunities for Brookfield to deploy its capital.

Insurance business in Wealth Solutions provides stable capital inflow for Brookfield to expand its assets under management.

Threats

Economic downturn or other macro factors like high interest rate may slow the amount of available capital to be managed by Brookfield

The good performance of index funds reduces the appetite of alternative assets provided by Brookfield.

Regulatory changes: Changes in regulations affecting the asset management or insurance industries could adversely affect Brookfield's business15. New regulations could increase compliance costs, restrict investment activities, or impact the profitability of Brookfield's wealth solutions business.

Investment risk: The capability for Brookfield to invest with a high level of return is a black box to investors. It is not certain that Brookfield can maintain its lead in the industry.

References

Brookfield Corporation Official Website

2024/11/21 Pershing Square Holdings Ltd. (PSHZF) Q2 2024 Earnings Call Transcript

2024/11/14 BN 2024 Q3 earnings

2024/09 2024 Brookfield Corporation Investor Day Presentation

Updates

2025/02/14 Valuation update with 2024 Q4 earnings

2024 Q4 Letter to shareholders

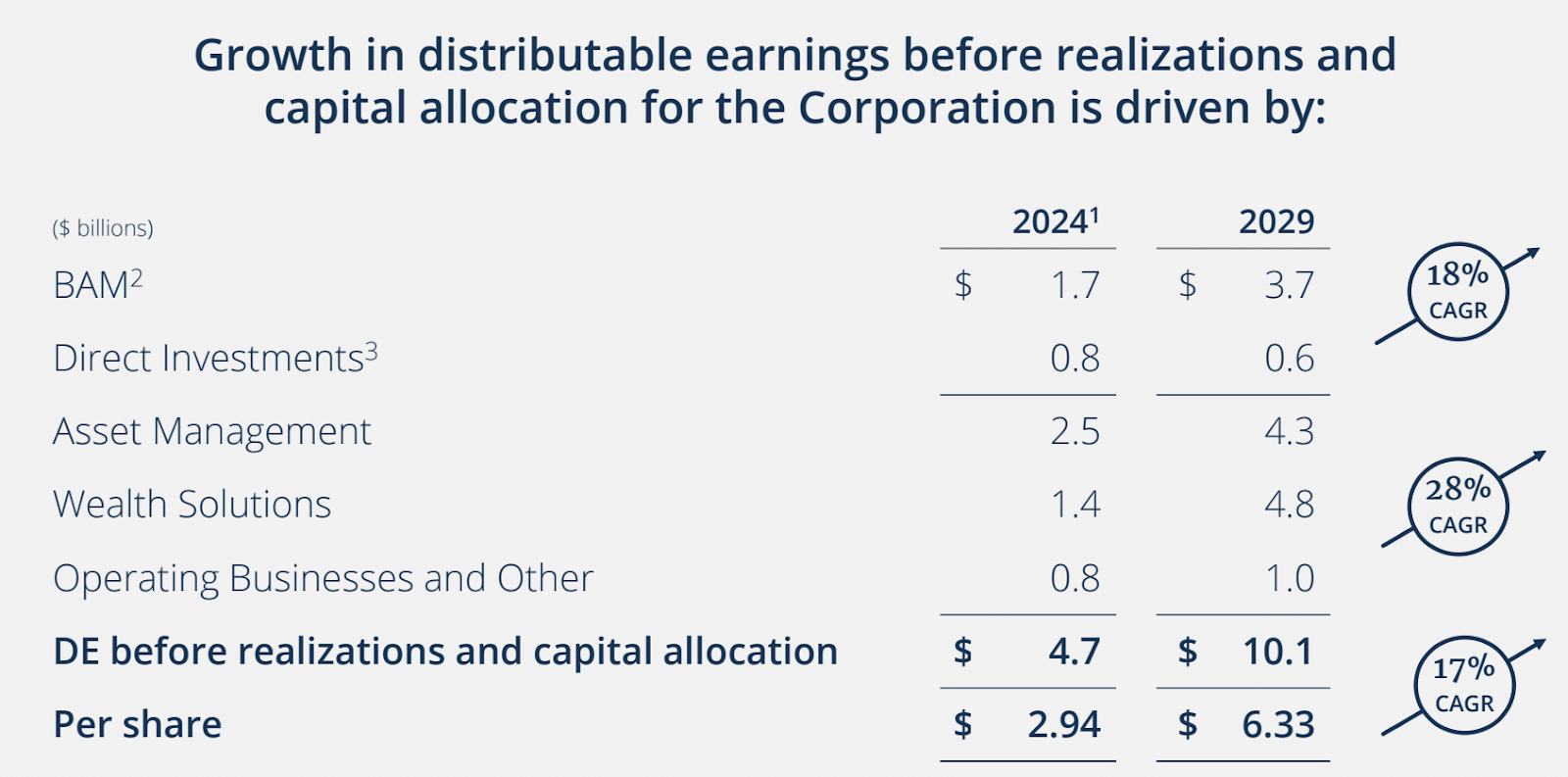

Good earnings result and on track to grow distributable earnings before realization by 15% annually for the upcoming years.

2024/12/13 Valuation

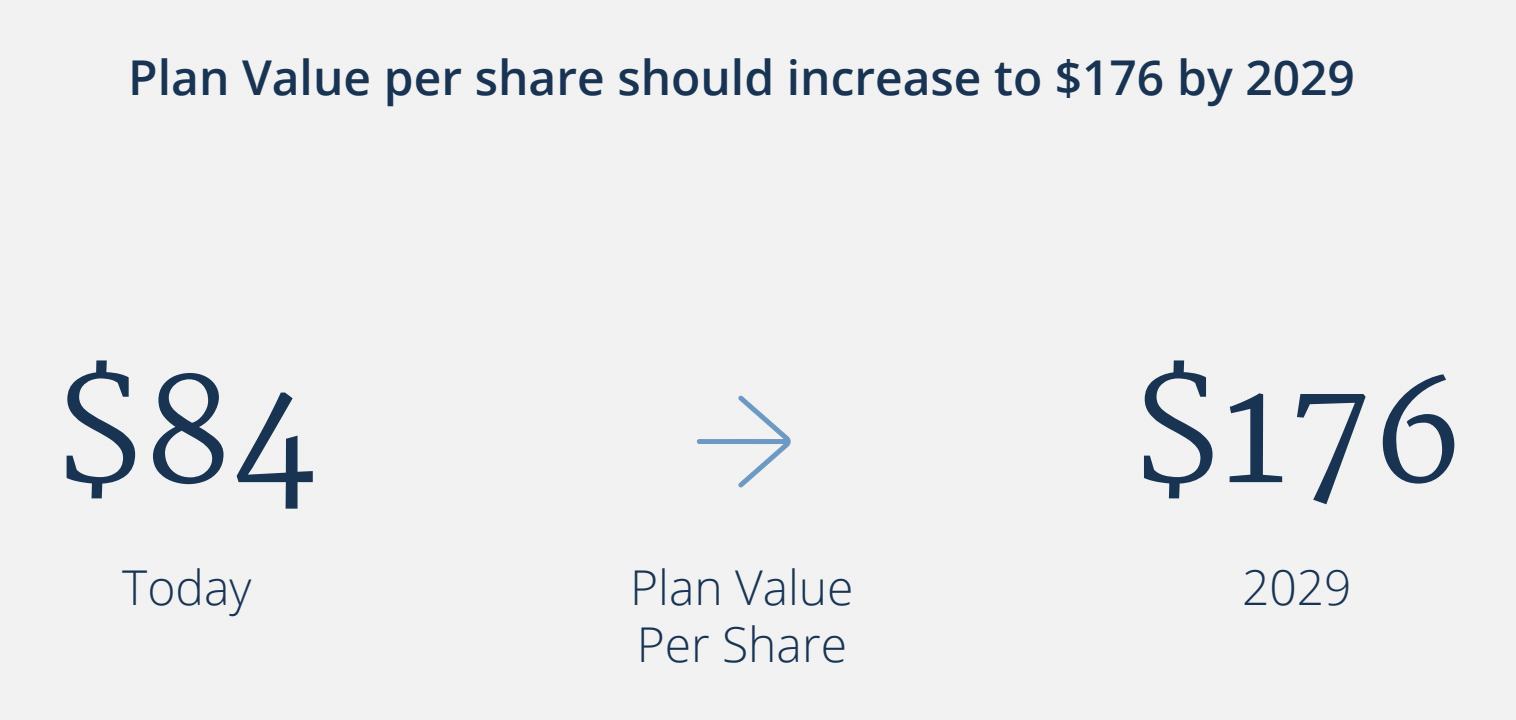

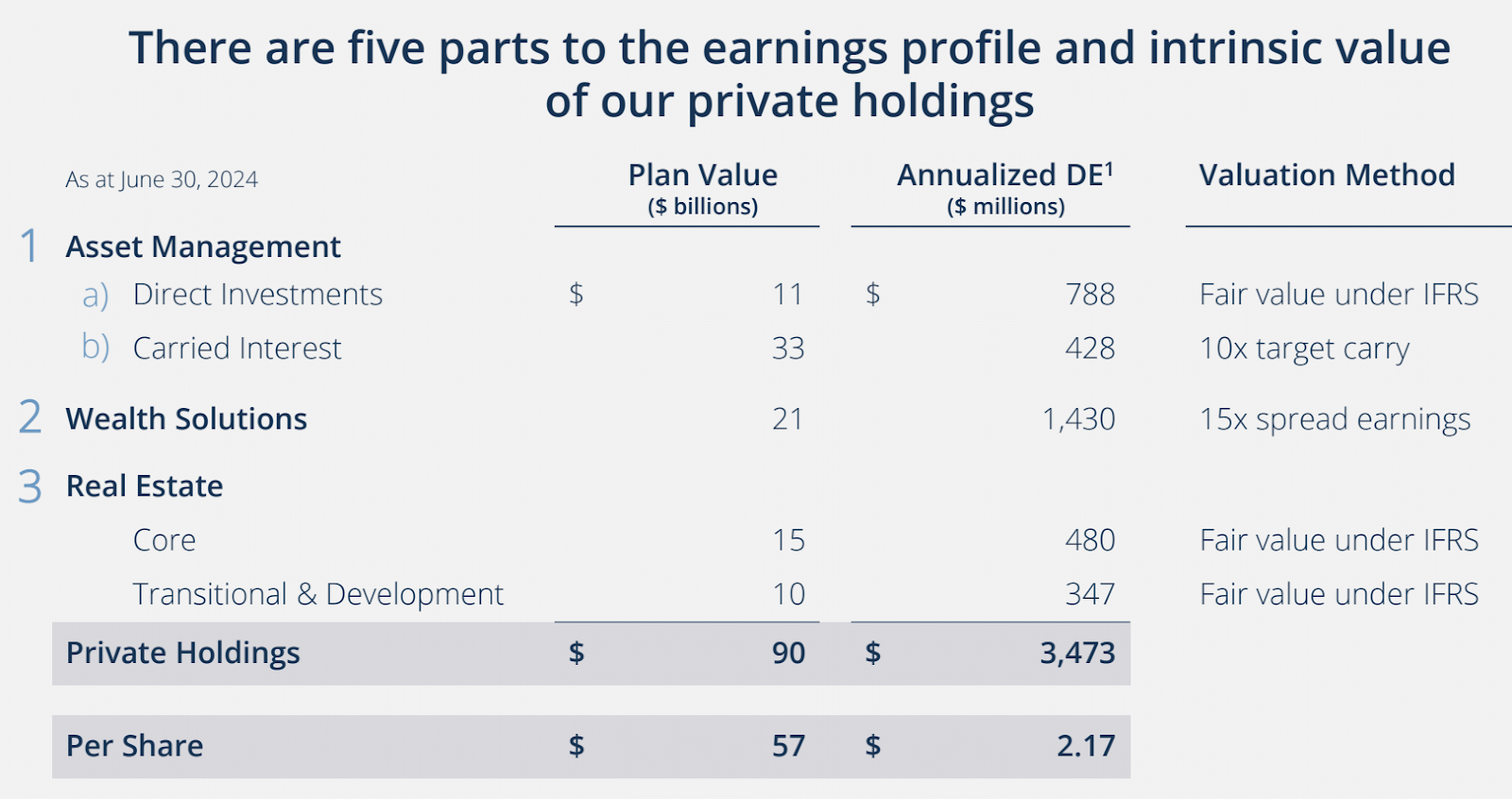

The management gives a plan value of $84 per share by 2024 Q2. They guided for $176 per share of plan value in 2029.

The plan value can be seen in the slides from the Investor Day:

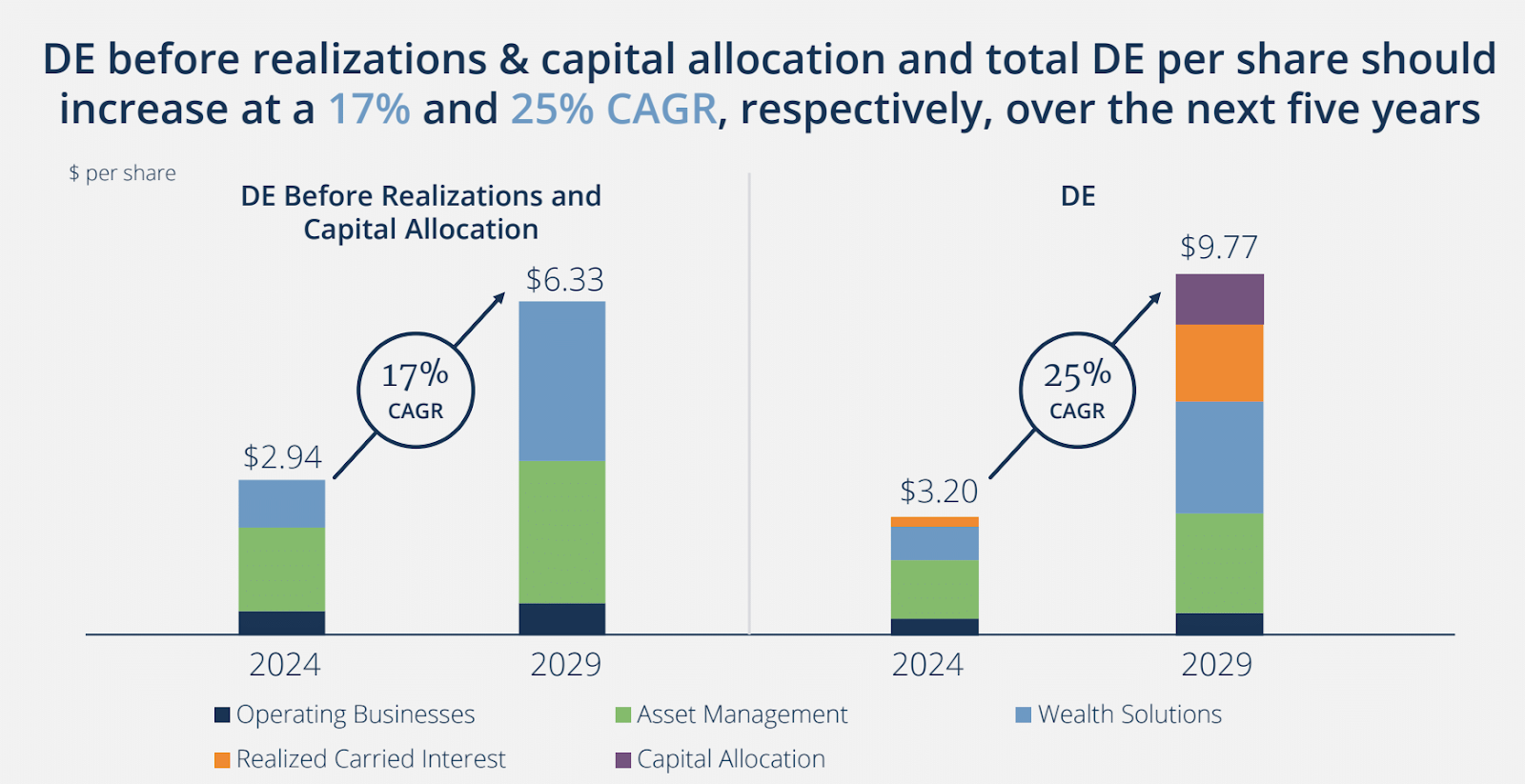

Distributable earnings of $3.67 per share for the TTM at 2024 Q2. The management guided for $9.77 per share in 2029.

The annual growth in both plan value and distributable earnings are higher than 15%, so one can easily get a satisfactory return with a conservative multiple of either measure.I would use a 20% discount for plan value, and a 20x on DE before realization, and 10x on DE from realization.

2024 Q3 per share data:

2024/11/21 Pershing Square Holdings comment on Brookfield Corporation

The following is the main investment thesis of Brookfield Corporation by Pershing Square Holdings (told by Bill Ackman and Charles Korn) from Pershing Square Holdings Ltd. (PSHZF) Q2 2024 Earnings Call. The share price of $BN on that day was about $57.

"they're an owner and operator and manager of critical infrastructure and assets which they would say powered the backbone of the global economy."

Brookfield generates cash flows from controlling ownership it has in a handful of these interrelated subsidiaries in various contractual cash flow streams. The most principal asset that they own comes from their 73% ownership they maintain in their publicly traded asset manager, called Brookfield Asset Management known as BAM.

"BAM is one of the world's preeminent alternative asset managers. And they derive a significant portion of their value from asset-light recurring management fee streams on $540 billion of long-duration internal and external capital that they manage. And BAM's success stems from deep investment expertise and a best-in-class track record in the areas of infrastructure, power, renewable energy, real estate, and credit...they own Oaktree as well."

"it's an investment focus that they have around three key themes which include decarbonization, digitization, and de-globalization and increasingly Brookfield, they find themselves at the center of accelerating investments in clean energy and transition, critical infrastructure and most recently artificial intelligence."

"we think BAM's fee earnings will nearly double through 2028 as they rapidly scale their fee-paying AUM to approximately $1 trillion, driving higher revenues which with strong operating leverage, will drive significant earnings growth."

"it has all the attributes of what we say is kind of a classic Pershing Square investment. It's simple, predictable, high quality, and a rapidly growing capital-light business. And simply put, it's Brookfield's crown jewel."

sum of the parts:

"the market is currently valuing BAM at 33 times earnings, which is a $66 billion asset at BN's 73% proportionate ownership worth roughly $41 a share in value to BN."

"when they spun out BAM retained a disproportionate share of the right to carried interest that BAM has on their long-term funds including 100% of carried interest from all funds which existed prior to 2023 and one-third claim on carried interest on all BAM funds thereafter."

"management has guided to $11 billion of cash flows over the next five years and $25 billion of cash flows over the next 10 years. We anticipate carry will stabilize in the $2.5 billion range within the next couple years, so more than a 5x multiple of the current cash flows"

"they receive dividends from $18 billion of equity ownership, BN maintains in a number of their publicly listed affiliate companies. These are tickers like BIP and BEP.

"they have cash flows from $11 billion that BN has invested in BAM's long-term funds which creates alignment of interest between BN and the limited partners in BAM's funds"

"they have a $24 billion real estate business which they own on balance sheet"

"they have this rapidly growing wealth and retirement solutions business"

"Brookfield has assembled a leading retirement and wealth solutions business which today manages approximately $115 billion of insurance float capital. And this business is focused on issuing long duration low-risk annuities which pair exceptionally well with Brookfield's asset composition which is focused on these real assets like infrastructure assets"

"The business is highly synergistic for the Brookfield ecosystem as BAM is the manager which invests the float on behalf of policyholders, which generates a capital-light and high-margin management fee stream for BAM, while BN generates earnings on the realized asset yield above the cost of insurance."

"This is referred to as spread earnings in the industry. Brookfield Wealth Solutions, this business is today generating $1.3 billion of earnings, but they have near term line of sight to $2 billion on a path to more than $3 billion over the coming years. And the business we note features very strong parallels to Apollo and KKR's highly successful similar strategies they've employed with Athene and Global Atlantic respectively."

"BN, the parent is today trading at roughly 15 times our assessment of earnings, which we view as a very low multiple in the context of a recurring cash flow stream that we estimate will more than double through 2028 to $10 billion plus, which is a 20% compounded growth rate."

"growth will be driven by the scaling of this wealth solutions business, a step function change in the contribution from carried interest, attractive teens plus growth in BAM's fee earnings and stable mid-single-digit growth across their other holdings. This rapid growth in earnings will also generate significant excess cash flows with we estimate approximately $25 billion of cash which Brookfield can use for buybacks or other intelligent capital allocation, which is nearly 30% of BN's current market capitalization."

"And when we look at the composition of Brookfield's 2028 cash flows, applying a mid-teens multiple weighted average multiple sum of the parts multiple, we anticipate shares are poised to more than double over the coming years. Now, I would also say that comparison however to publicly traded peers such as Blackstone, but more significantly KKR and Apollo would imply very significant valuation upside relative to what I just mentioned and as an observation."

"today KKR and Apollo are trading at 27 times and 22 times earnings. And what's interesting is we think that KKR has actually very similar composition of cash flows as compared to BN. If you were to stack them up on what they're going to look like in 2028 between spread earnings, fee earnings, and carried interest.

Whereas when you look at Apollo, Apollo actually generates two-thirds of their earnings from the spread insurance-based business, which you could argue is probably the lowest quality fee stream and yet they're trading at 22 times kind of consolidated earnings."

"Brookfield is anchored by its look through value to BAM, which I mentioned is worth more than $41 a share. If you add the $18 billion they own in their other publicly traded affiliates"

"So, there's public marks for these entities. It basically covers almost the entire market cap of the parent BN, at which point we think you're getting basically $50 billion of value for free, which includes the carried interest claim, the entire wealth solutions, this insurance business that they have and a $24 billion real estate portfolio."

"in closing, we think Brookfield is a high-quality asset-rich, rapidly growing business with an attractive earnings outlook. And while the stock's risen actually more than 40% relative to when we started acquiring our position, we continue to believe BN is very undervalued and anticipates strong future returns from here."

"And index inclusion has become a critically important driver of valuation, I would say for or achieving sort of the upper band of valuation for US-listed companies and Brookfield is certainly aware of this issue, they're in the process now of moving the headquarters of their BAM to New York from Toronto and making that business eligible ultimately to be purchased by index funds."

2023/06/15 Brief analysis

With an IFRS book value of $52.36, Brookfield Corporation is trading at a 37% discount to book. With their asset management business and reinsurance company, they will be able to continue to earn stable cash flow to deploy into their attractive return opportunities from real estate and infrastructure. Mohnish Pabrai believes Brookfield has the best alternative management DNA (video, full interview), so I have no doubt this is a great company to own for the long run.

With their asset management business growing 10-15%, and their holdings in various real estate and infrastructure earning 10-20% annual return, it's a stock that can achieve an annual return of 15% easily given the huge discount to book.

No comments:

Post a Comment