Business Description

Alibaba Group Holding Limited (NYSE: BABA) is a Chinese multinational technology company specializing in e-commerce, retail, Internet, and technology. The company was founded in 1999 by Jack Ma and has since grown to become one of the largest e-commerce companies in the world. Alibaba operates a variety of online marketplaces, including B2C: Tmall, and AliExpress; B2B: Alibaba and 1688, Alimama; C2C: Taobao. It also has a small footprint in physical retails with supermarkets like Hema and Sun Art and department store Intime. The company also provides cloud computing, digital media, and logistics services. Finally, it owns ⅓ of Ant Financial, which is one of the top Fintech companies in the world.

Alibaba's mission is to "make it easy to do business anywhere." The company's vision is to "be the world's leading technology infrastructure company."

I am confident in Alibaba's long-term prospects, considering its pioneering role in China's e-commerce, digital payments and cloud service landscape. The company has overcome significant challenges, such as addressing credit, logistics, and bureaucratic hurdles in a developing nation, to establish itself as a dominant force in China's digital economy.

Moreover, Alibaba's digital payment platform, Alipay, stands out as a world-class offering. While Alipay trails WeChat Pay in terms of transaction volume, its role in educating merchants and institutions about digital payments cannot be overstated. Alipay's efforts have paved the way for WePay's success and facilitated the widespread adoption of digital payments across China, streamlining complex regulations and reducing transaction costs.

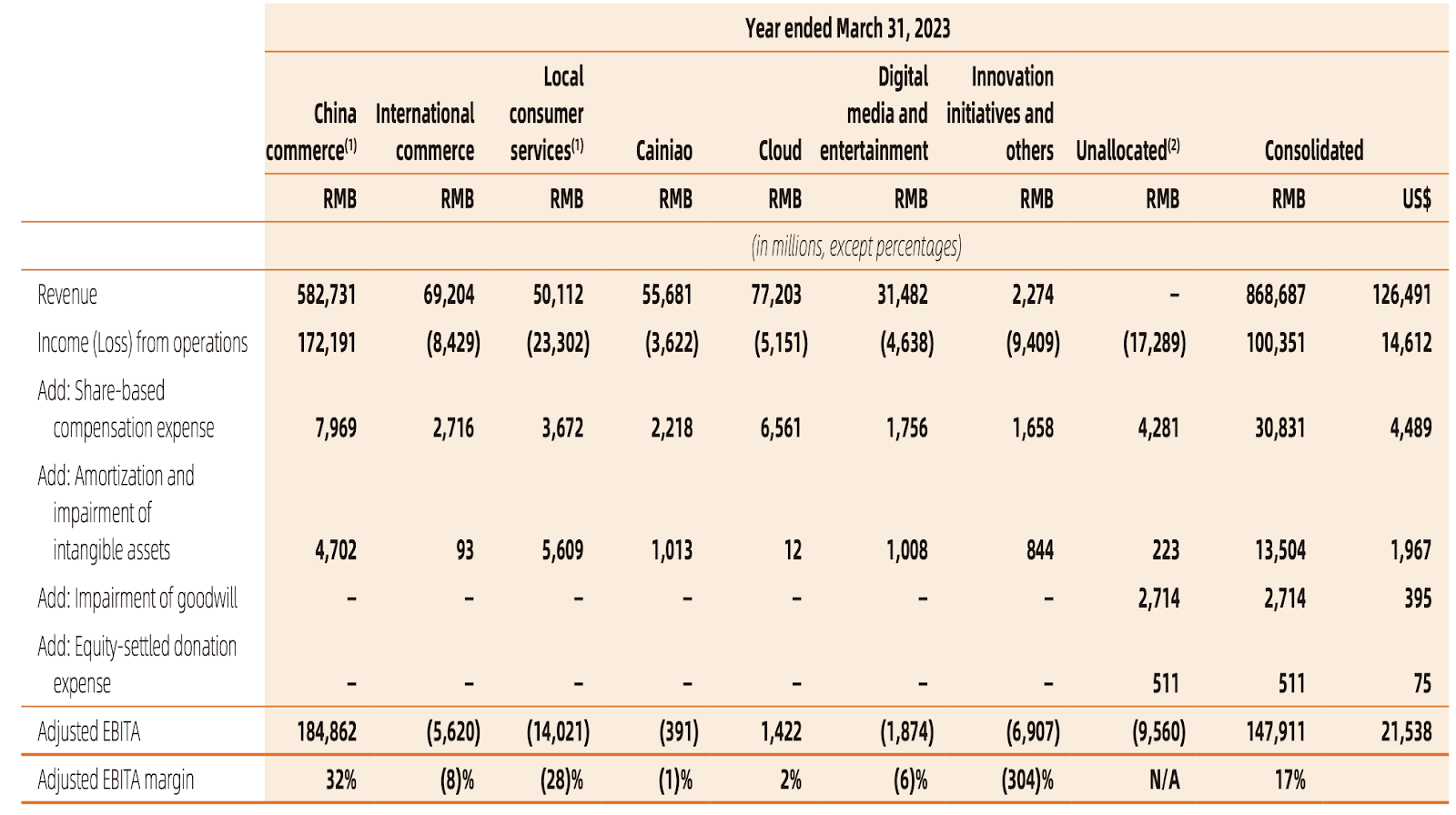

In the 2023 result, we can see that most of the revenue and income of Alibaba comes from China commerce. I expect the Cloud segment will be a significant contributor eventually, similar to the trajectory of AWS to Amazon.

It is very comparable to Amazon in terms of the lines of businesses. In fact, I think Alibaba is superior in a lot of aspects.

SWOT analysis

Strengths

Largest scale of the world in e-commerce including Taobao and Tmall marketplaces which allows for low distribution cost for merchants.

The large e-commerce scale enabled the development of advanced infrastructure including logistics, computing infrastructure, payments, artificial intelligence, and various other researches. It's pretty much the play book of Amazon that allows large scale infrastructure having its own to be the first customer, e.g. AWS.

Strong and stable cash flow generation from the e-commerce business allows long-term and ambitious projects to be funded by the parent company.

The ecosystem built around e-commerce, video streaming services, and local services (e.g. food delivery) enabled each other by channeling traffic to each other, while creating additional values to users.

Own ⅓ of Ant Financial, one of the top two fintech companies in China.

Top-notch technology stack among all China-based companies.

Weaknesses

The ecosystem got weakened due to the China government regulations.

Weak execution in e-commerce caused a crack in Taobao and Tmall dominance in e-commerce. Pinduoduo may overtake Taobao in the long-tail market.

The cloud business was slowed down by China government regulations and the US technology export ban.

Opportunities

The recent reorganization of the business units in March, 2023 may light up the entrepreneurial fire of its employees, while the focus on shareholder returns with dividends and shares buyback reduce the risk of shareholders.

Counterattack on Pinduoduo at the long tail e-commerce market can stabilize the loss of market share.

Greater invention and technology from industry leading research can lower the cost of delivery that leads to cost advantage in e-commerce and local services.

Alibaba's Taobao and Tencent's WeChat have joined hands, so that Taobao advertising traffic can come from WeChat more seamlessly.

Threats

Pinduoduo is a great threat to Taobao. In the international market, Temu by Pinduoduo also beats Aliexpress. There is no sign that Alibaba can stop the market share loss at this point due to Pinduoduo's counter-positioning on the long-tail e-commerce market.

Geopolitical risk in China. From China government regulations, they disproportionately hurts Alibaba because of its large scale footprint in various sensitive industries: fintech, e-commerce, cloud, infrastructure. From the international countries, technology export ban led by the US and trade wars between China and the US can hurt Alibaba's e-commerce and cloud businesses.

References

Alibaba group official website

September quarter 2023 result, transcript

Updates

2023/12/04 Valuation

Sum of the parts analysis:

China Commerce: 2022 (fiscal year 2023) EBITA: $184 billion CNY, which is $25 billion USD. Assuming a EBITA multiple of 5 (Macy's, a declining department store, has such multiple), that part is worth $125 billion.

Cloud: $10 billion USD revenue. Using a 10x multiple gets a valuation of $100 billion.

⅓ of Ant Financial: $20 billion

International commerce + Local consumer services + Cainiao + Digital Media and entertainment have a total of about $30 billion USD in revenue. Assuming a cheap 2x multiple gets $60 billion.

Net cash by the end of Sept, 2023: $63 billion

There are 2.5 billion ADS outstanding, so these 5 parts alone already totaled (125+100+20+60+63)/2.5 = $147 per share.

Then there are also $67 billion US dollars ($26.8 per share) in equity securities and other investments.

No wonder Charlie Munger started the position of Alibaba when it was trading at over $200.

Another way to evaluate Alibaba is by using a free cash flow multiple. It earns $27 billion in the 2023 fiscal year. Using a 10x multiple gives it at least a $270 billion market cap, or $108 a share. Then you can add that $63 billion net cash ($25 per share) for a total valuation of $133 a share of ADS, give or take.

That being said, given the unpredictable geopolitical risk of China, Alibaba will always be a small part of my portfolio no matter how cheap it is.

No comments:

Post a Comment