Put in $2000, then purchased:

$400 for APO

$400 for BN

$400 for PAX

$300 for GLDM

$300 for TSLA

$200 for BTC

$327.76 for AHH

Also sold all GTY and WPC to buy $2173.5 of NNN.

There were quite a lot in this update. First of all, I increased my positions in alternative asset managements as usual, because they were still cheap with their business model having sticky recurring revenue, valuating at P/E around 20, having 10-15% annual earnings per share growth and token dividends.

AHH is still cheap and getting cheaper every day with over 8% dividend yield using my valuation method on 2024/09/07:

There is some risk in its high debt load, but I believe its equity issuance in September should have de-risked it enough.

Now, talk about new symbols. I started a position in Tesla (TSLA) after seeing its new FSD version 13 is getting closer to fully autonomous driving. Elon Musk, again, said Robotaxi will start testing in this year second half. I believe it has a fair chance to catch up on competitors and eventually be the first to provide scalable Robotaxi services in terms of cost and road coverage. This investment belongs to Shut Up and Hodl Basket given it relies on trusting Elon Musk's words while the company's financial metrics currently do not justify a valuation more than $200 billion (its market cap is ~$1.15 trillion currently). I have a small writeup for the stock.

Gold (thru GLDM) and Bitcoin (thru BTC) are two other new symbols belonging to Shut Up and Hodl Basket. It's mostly for me to hedge against long-tail macro event. I also wrote two pieces for Gold and Bitcoin to explain my thought further.

Finally, I sold GTY and WPC in exchange for NNN. They are all triple-net lease REITs, but I like NNN a bit more due to its long track record in FFO per share and dividend increase for 35 years, its conservative balance sheets management, and a consistent simple strategy in acquiring retail properties which tend to have stable cash flow (writeup). It doesn't have the risk of getting disrupted by EV revolution in the case of GTY, and its management has a better track record than WPC. To be honest, I am not sure whether I need to swap WPC for NNN. WPC is not bad, and it's also very safe with a little bit higher dividend yield. I was mostly fixated on eliminating a REIT symbol given I have too many REIT stocks already. With my philosophy of avoid selling for this portfolio, I might as well keep WPC. Anyway, what was done was done.

Transactions

Recent and upcoming dividend distributions

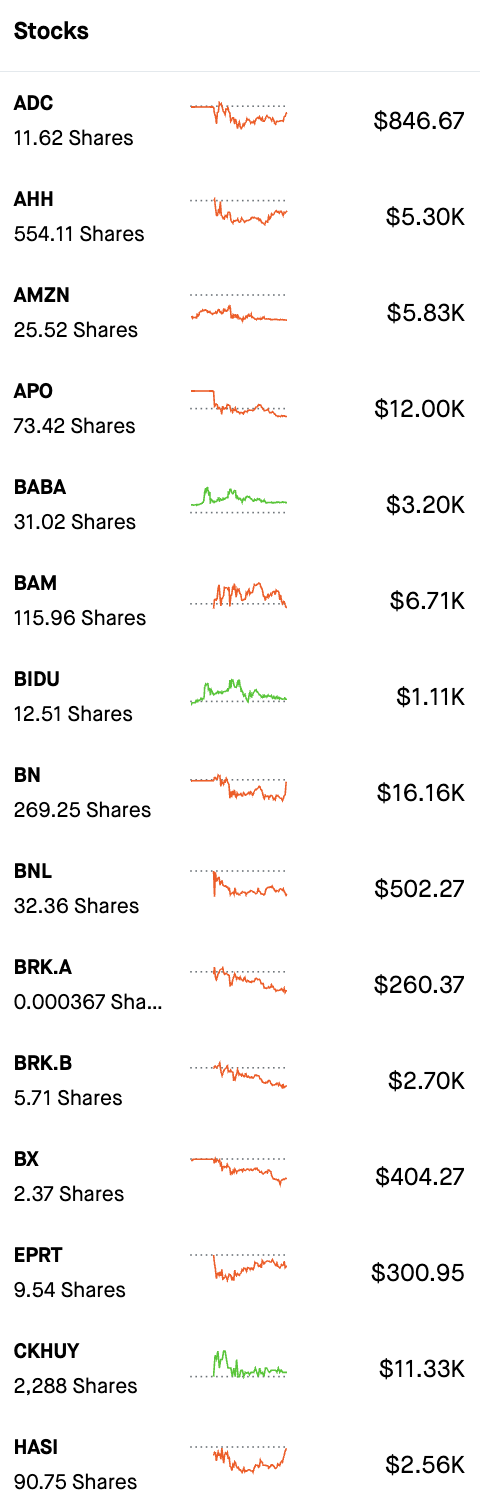

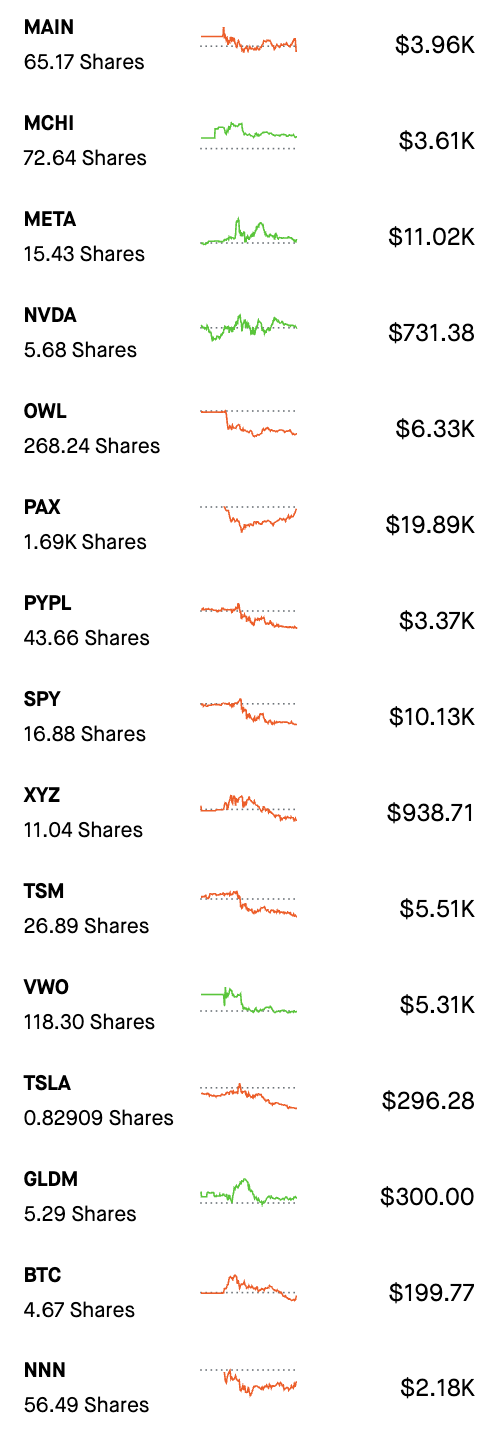

Portfolio

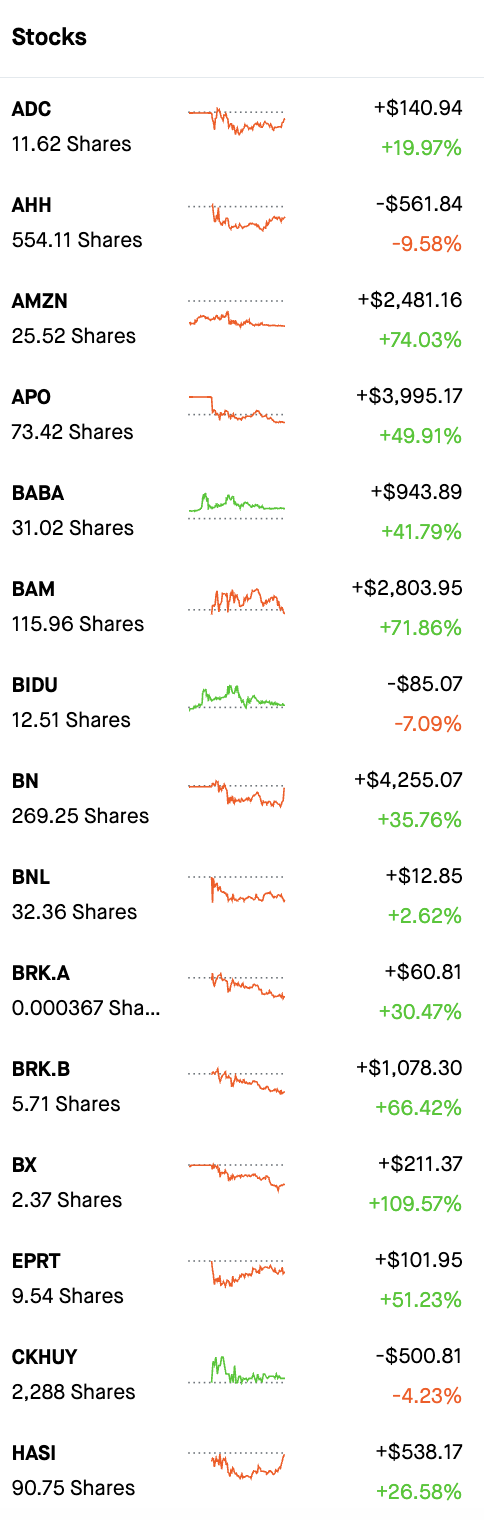

All-time return:

One-year return:

Portfolio IRR (calculation): 24.85% (correct as of 2025/02/08)

Approximated IRR for an SPY-only portfolio: 18.69% (correct as of 2025/02/08)

Individual holdings:

Breakdown by categories (real-time):

All-time returns for individual holdings:

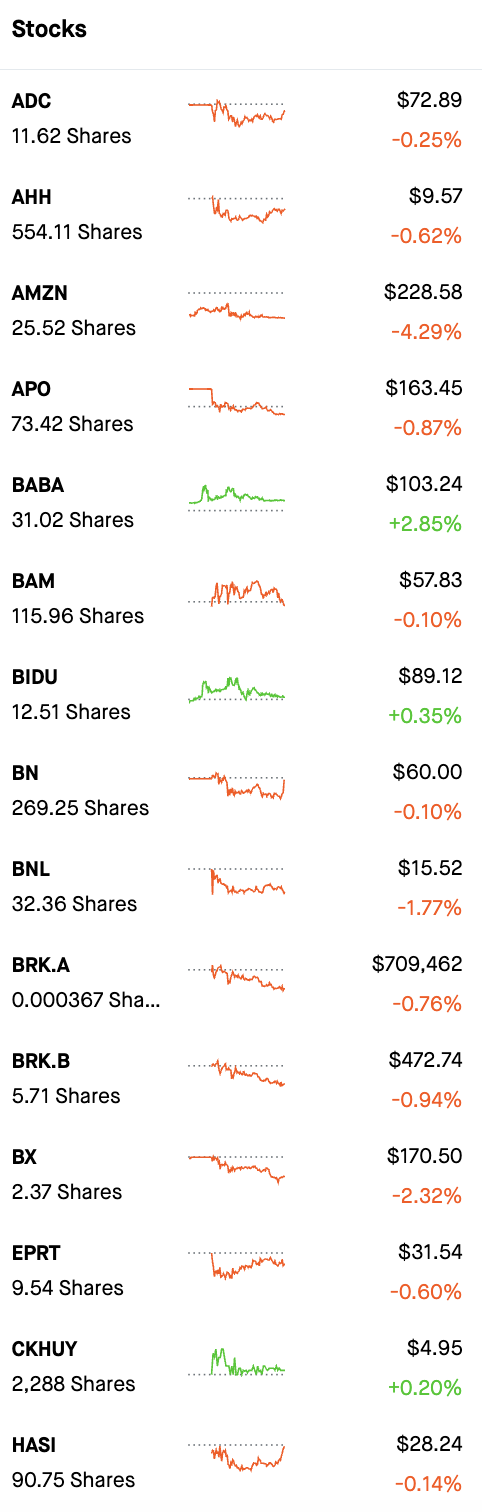

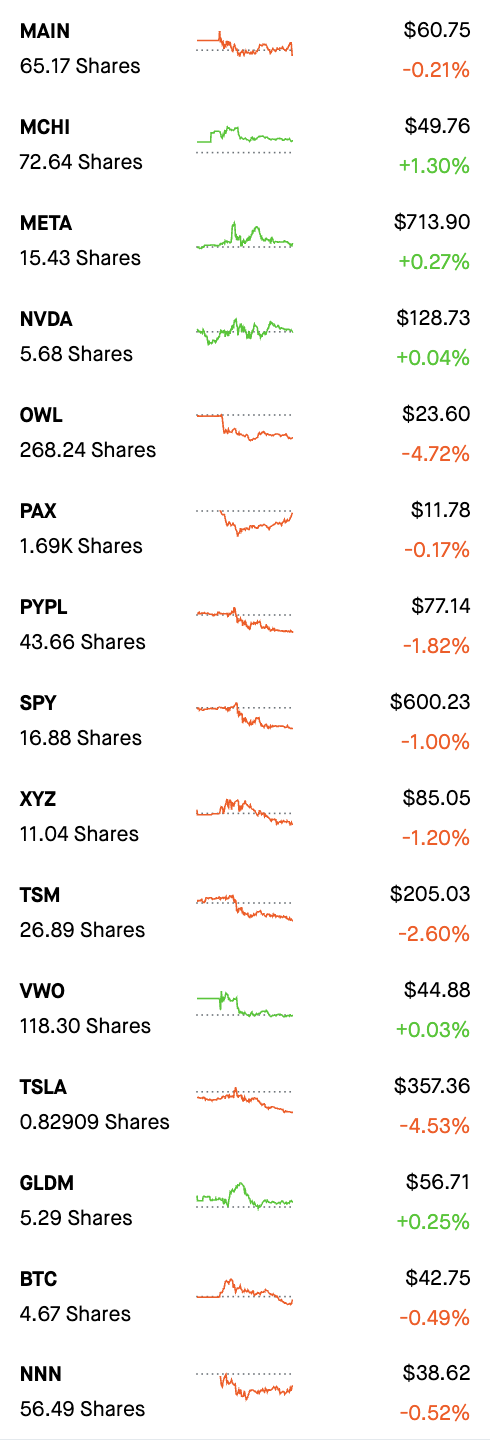

Last prices:

Portfolio holdings conviction

The convictions in the table below reflects my current opinions and will guide the future contribution of additional investment to existing holdings. Stocks not inside the table are stocks with subpar return on equity that will be very unlikely to receive more contributions from new money (there can be exceptions for very cheap stocks).

Conviction in long-term prospects means how much I believe a company would match or outperform the market (e.g. S&P 500) in the long run. Valuation matters so the conviction generally corresponds to the neutral rating of Valuation. It has the following ratings: weak, moderate, strong

Valuation: overvalued, slightly overvalued, neutral, slightly undervalued, undervalued, greatly undervalued

Brief comments on individual holdings

ADC

Agree Realty is one of the lowest leverage triple-net lease REITs with a debt to EBITDA ratio of 4.9x. Its tenants are mostly investment grade (67%) retailers and restaurants. At the worst time of 2021, it collected 95% of the rents, which shows the quality of its assets.

One special thing about Agree Realty is its 14% portfolio in ground leases, which has low default risk, low cash flow, with short-term inflation risk, but long-term stable return. It diversifies the risk portfolio of the company.

Its acquisition and disposition ratio is 4.2% in 2021. The ratio is kept low for the past, which again, shows the quality of the assets, so that it does not have to sell many non-performing assets.

XYZ

Brief analysis and latest updates here

PYPL

Analysts expect Paypal 2023 EPS to be $4.94, and will grow more 15-20% annually for a few years. Its top line will grow at a high single digit as well. 2023 P/E ~ 13 is quite attractive. Paypal's economic moat did not change recently. Its neutral position in payments is a good counterposition for big competitors like Apple Pay, Google Pay, Visa, Mastercard, Zelle, etc. It's OS and payment network neutral. As a case in point, Paypal was accepted as a payment on Amazon.

Short-term catalysts are continuous growth of users in Venmo, shopping super app, and the cost cutting measure to make the company more efficient. The stock price is depressed now only because the market worries about its short-term growth.

META

Global Monthly Active User (MAU) above 2.8 billion. Facebook is the biggest social network in the world. There will always be people buying Facebook/Whatsapp/Instagram.

The economic moat is weakened by Tiktok, but Tiktok is not really a social network that connects users who are familiar with each other, but another variant of youtube, so Facebook is still the top dog in social networking, although user time spent is definitely hurt.

Given Facebook's investment in VR; optional values in Facebook dating, and Facebook shops; Facebook Pay and Messenger have good monetization potential; Instagram has a unique position for people to express themselves; the improvement in Ads Infra to compensate for the loss in Apple App Tracking Transparency, I believe Facebook will come back. Long term annual growth of 15-20% in earnings should not be a problem.

BRK.B

Berkshire Hathaway in the current form was found by my idols, Warren Buffett and Charlie Munger. I will try to buy more if it's not very expensive.

AMZN

Brief analysis and latest updates here

OWL

Blue Owl Capital is an alternative asset management company, similar to Blackstone. Its focus is on direct originations of loans to private-equity backed and non-sponsored companies (middle-market and upper-middle-market companies). It has a net leases real estate platform. It also provides long-term minority equity and financing to private capital investment managers. A majority of the company's assets are funded by permanent capital, so it does not have withdrawal risk. Most of its earnings come from recurring fees from asset management without performance consideration, so the earnings stream is quite stable. Given it acquired STORE Capital (STOR) recently at a decent price, the management is very good.

Equity compensation related expenses were about 35% of DE that got added back into GAAP when getting DE. Its "true" EPS is about $0.1 per quarter, or about $0.4 in 2023. The P/E is about 30, not cheap, but not very expensive considering its growth is 15-20% annually. Another way to look at it is that its dividend yield is about 4.5%, and it's growing in double digits for at least 3+ years, which makes it quite attractive.

APO

Apollo specialized in distress situations, which reduced the number of competitors. Its famous slogan is purchase price matters, which shows how price conscious they are in picking investment. It has another slogan "we want 25% of everything and 100% of nothing on the asset", which is a goal post of the company about engaging in a lot of asset managing transactions even for other asset managers. It's a good way to position the company to have a large adjustable market. Their use of reinsurance company, Athene, helps them to grow assets under management effortlessly as well.

Expected 2023 EPS is $6.61, so P/E around 12, pretty cheap with an expected growth of 10-15%. 2.5% dividend yield helps a bit as well.

BN

Brief analysis and latest updates here

BAM

The pure asset management company part of the Brookfield Corporation. With BN, BAM can grow its asset under management (AUM) easily. Oaktree Capital, founded by the famous Howard Marks, is part of it, so it's very reputable.

The management has already indicated they are locked in to grow its cash flow 15% annually for the next field years. Its management fees do not rely on performance that much, so they are stable. With an expected 2023 EPS of $1.39, P/E 25 is not cheap, but with the help of 3.8% dividend yield (close to 100% payout, thanks to the asset light business model), there is a fair chance the stock can return 15% annually.

BX

A very reputable company in real estate. Its management fees rely on performance much more than Brookfield, but Blackstone has a track record, so I am not too worried about it.

Expected 2023 EPS is $4.36, P/E ~ 21. A 3.5% dividend yield with expected annual growth of 10-15%, this stock can potentially get a 15+% return in the long run.

CKHUY

CK Hutchison Holdings (OTC: CKHUY, SEHK: 0001) is a diversified conglomerate with interests mostly in telecommunications, retail, ports, infrastructure, and energy. The company was founded in 1979 by Li Ka-shing, one of Asia's richest men.

CK Hutchison is a well-managed business with a long history of profitability. The company has a strong track record of generating free cash flow, which it has used to invest in growth mostly by M&A, and return to shareholders through dividends and share repurchases.

CK Hutchison's businesses are all essential services that are not easily disrupted by new technologies or competition. This gives the company a moat that protects its profits and allows it to generate stable cash flow over the long term.

It is trading at $6/$18 ~ 33% of book value, P/E ~ 8, and a dividend yield of over 6%. The ADR costs probably $0.05-$0.1, which unfortunately is quite costly for lowly-priced stock like CKHUY.

HASI

Brief analysis and latest updates here

AHH

Brief analysis and latest updates here

EPRT

Brief analysis and latest updates here

MAIN

Brief analysis and latest updates here

BABA

Brief analysis and latest updates here

PAX

Brief analysis and latest updates here

BNL

Brief analysis and latest updates here

BIDU

Brief analysis and latest updates here

NVDA

Brief analysis and latest updates here

TSM

Brief analysis and latest updates here

TSLA

Brief analysis and latest updates here

NNN

Brief analysis and latest updates here

GLDM

Gold Brief Investment Thesis (for GLDM)

BTC

Bitcoin Brief Investment Thesis (for BTC)

SPY, VWO, MCHI

ETF Brief Descriptions and Updates