Sold all PLTR shares, then used the proceeds to purchase:

$3500 for BN

$4000 for PAX

$1167.84 for HASI

Palantir (PLTR) increased by more than 300% this year. It's a great company, but is it that great?

I sold $PLTR at about $74. PLTR is expected to earn $0.38 in 2024, and $2.02 9 years later in 2033. That means it's trading at P/E = 36 using 2033 earnings!

PLTR had a weighted average of about 2.46 billion diluted shares outstanding in 2024 Q3. The market cap is then 2.46 billion * $74 = $182 billion. It's expected to have $2.79 billion revenue in 2024, and $12.3 billion in 2033. That is a P/S of 14 using 2033 numbers, and 65 using 2024 numbers. It looks pretty expensive even with 20% annual growth. But let's dream a little bit here. We assume PLTR can have as much revenue as today's Lockheed Martin's revenue in 10 years...

I use Lockheed Martin because PLTR in some way is limited by how much pro-US governments are willing to spend. Given LMT's track record, I would say the best PLTR can do in 10 years (i.e. 2034) would be as great as LMT today. LMT is expected to have $74 billion in 2025. Let's say PLTR can achieve 20% profit margin (IBM, a company with a similar business model, only has 10% profit margin), and let's give it a 30x earnings multiple. PLTR's market cap in 2033 (P/E should be forward looking, so 2033's valuation should be based on 2034 numbers) would be $74 billion * 0.2 * 30 = $444 billion. The IRR would then be (444/182)^(1/9) - 1 ~ 10%. So even with all these big assumptions for PLTR, the expected return is just 10% annually for 9 years. If I use a discount rate of 15%, my expected fair value today for PLTR with the same big assumptions would be 444/(1.15^9) = $126 billion in market cap, which is $51 per share, or 30% below $74 per share, the price that I sold.

I am reluctant to sell a stock based on valuation, but PLTR is so overvalued today that I decided to sell it to buy some other stocks with much better value.

BN and PAX are two of my highest conviction stocks, so I put most of the sales proceeds into them. I diversified by choosing a dividend stock, and HASI fits the bill given its high dividend, potential 5-10% growth, and its defensive nature that invests in contractual cash flow from renewable energy generation.

My portfolio now has over 40% in alternative asset managers. I am fine with that given their business model has stable recurring revenue, and the expected annual growth is 15%+, trading at P/E of 15-30 (mostly at 15-20).

Transactions

Recent and upcoming dividend distributions

Portfolio

All-time return:

One-year return:

Portfolio IRR (calculation): 24.87%

Approximated IRR for an SPY-only portfolio: 19.04%

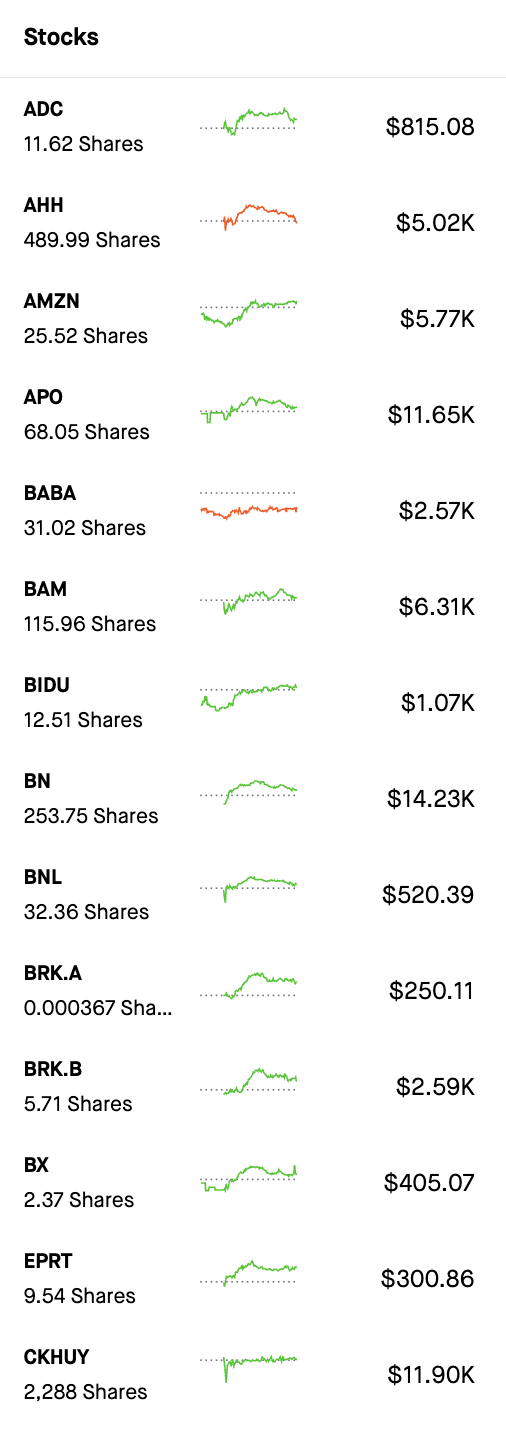

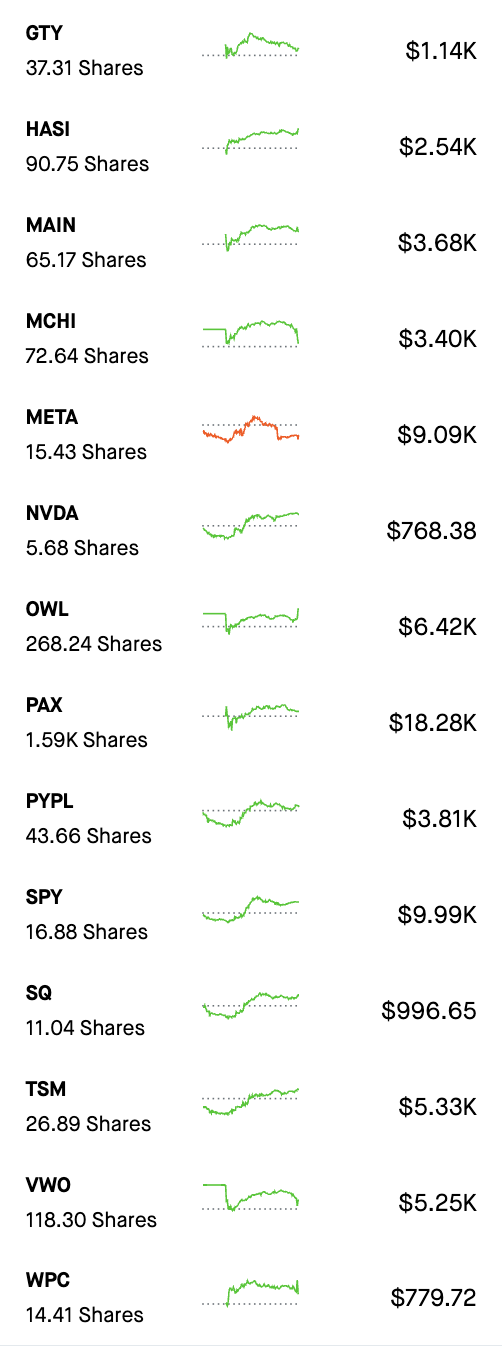

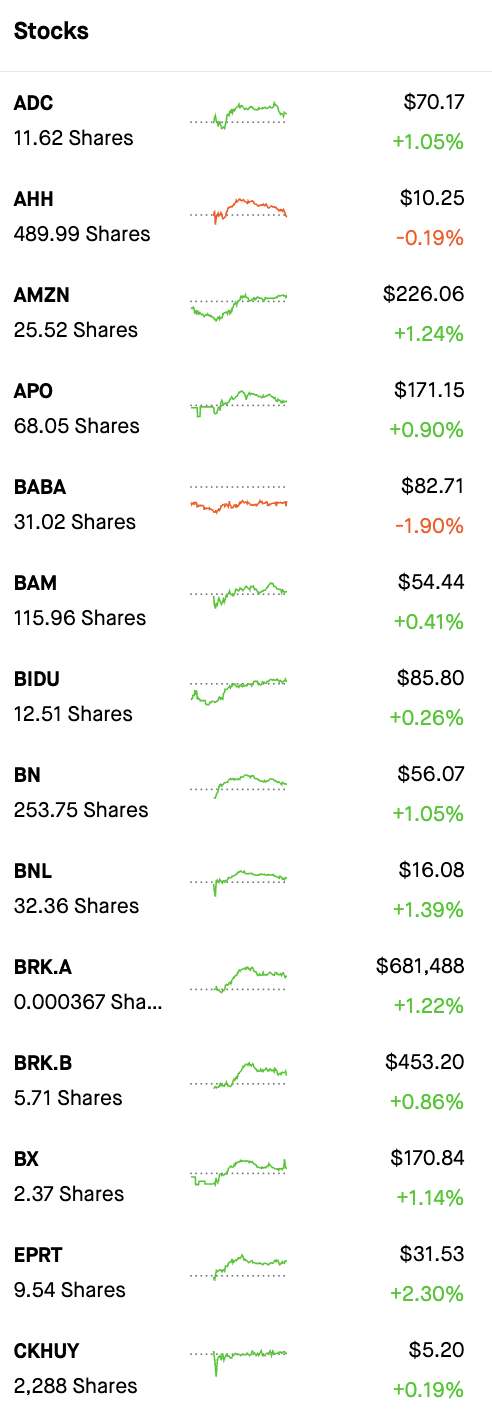

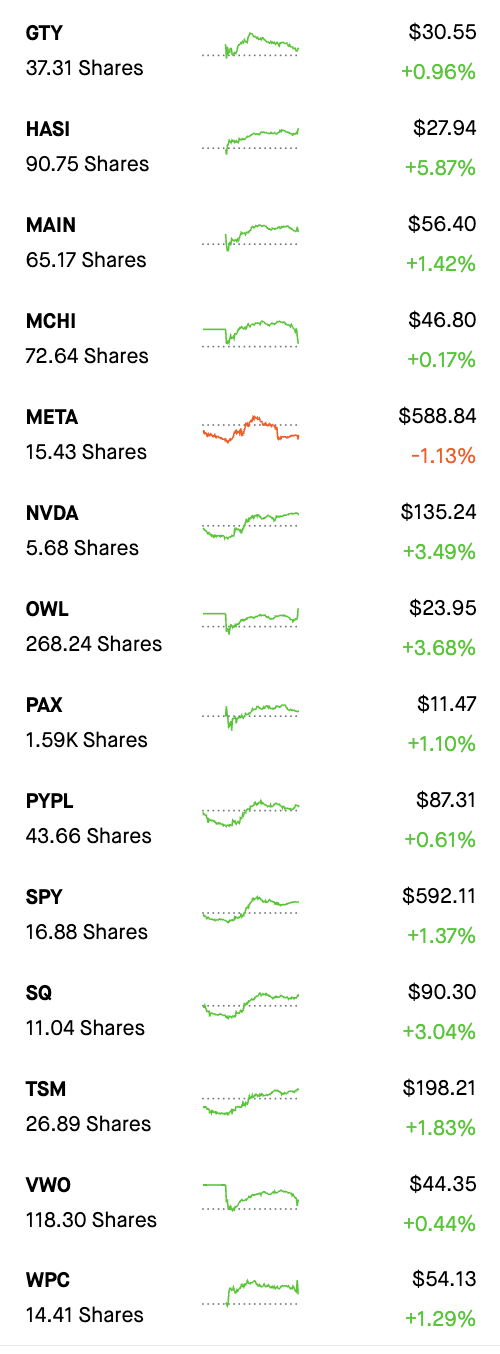

Individual holdings:

Breakdown by categories (real-time):

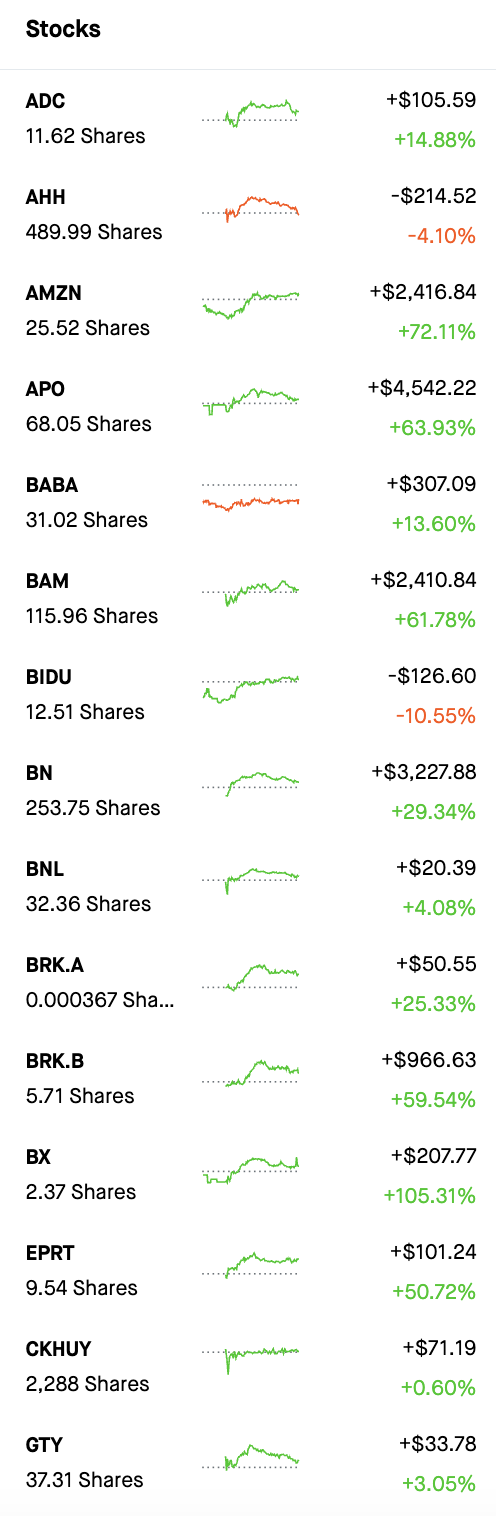

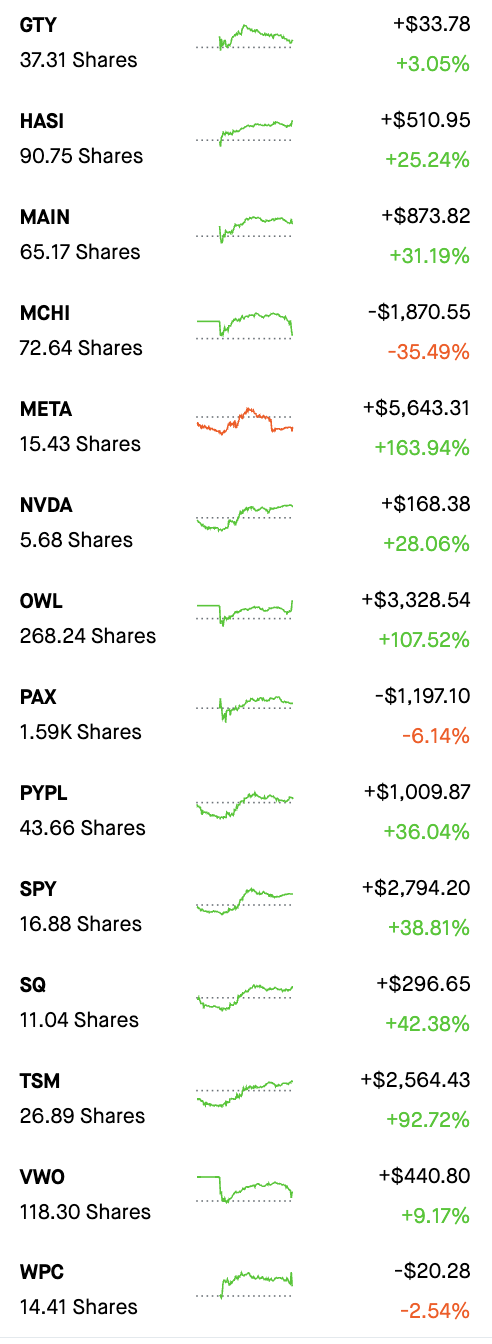

All-time returns for individual holdings:

Last prices:

Portfolio holdings conviction

The convictions in the table below reflects my current opinions and will guide the future contribution of additional investment to existing holdings. Stocks not inside the table are stocks with subpar return on equity that will be very unlikely to receive more contributions from new money (there can be exceptions for very cheap stocks).

Conviction in long-term prospects means how much I believe a company would match or outperform the market (e.g. S&P 500) in the long run. Valuation matters so the conviction generally corresponds to the neutral rating of Valuation. It has the following ratings: weak, moderate, strong

Valuation: overvalued, slightly overvalued, neutral, slightly undervalued, undervalued, greatly undervalued

Brief comments on individual holdings

ADC

Agree Realty is one of the lowest leverage triple-net lease REITs with a debt to EBITDA ratio of 4.9x. Its tenants are mostly investment grade (67%) retailers and restaurants. At the worst time of 2021, it collected 95% of the rents, which shows the quality of its assets.

One special thing about Agree Realty is its 14% portfolio in ground leases, which has low default risk, low cash flow, with short-term inflation risk, but long-term stable return. It diversifies the risk portfolio of the company.

Its acquisition and disposition ratio is 4.2% in 2021. The ratio is kept low for the past, which again, shows the quality of the assets, so that it does not have to sell many non-performing assets.

SQ

Brief analysis and latest updates here

PYPL

Analysts expect Paypal 2023 EPS to be $4.94, and will grow more 15-20% annually for a few years. Its top line will grow at a high single digit as well. 2023 P/E ~ 13 is quite attractive. Paypal's economic moat did not change recently. Its neutral position in payments is a good counterposition for big competitors like Apple Pay, Google Pay, Visa, Mastercard, Zelle, etc. It's OS and payment network neutral. As a case in point, Paypal was accepted as a payment on Amazon.

Short-term catalysts are continuous growth of users in Venmo, shopping super app, and the cost cutting measure to make the company more efficient. The stock price is depressed now only because the market worries about its short-term growth.

META

Global Monthly Active User (MAU) above 2.8 billion. Facebook is the biggest social network in the world. There will always be people buying Facebook/Whatsapp/Instagram.

The economic moat is weakened by Tiktok, but Tiktok is not really a social network that connects users who are familiar with each other, but another variant of youtube, so Facebook is still the top dog in social networking, although user time spent is definitely hurt.

Given Facebook's investment in VR; optional values in Facebook dating, and Facebook shops; Facebook Pay and Messenger have good monetization potential; Instagram has a unique position for people to express themselves; the improvement in Ads Infra to compensate for the loss in Apple App Tracking Transparency, I believe Facebook will come back. Long term annual growth of 15-20% in earnings should not be a problem.

BRK.B

Berkshire Hathaway in the current form was found by my idols, Warren Buffett and Charlie Munger. I will try to buy more if it's not very expensive.

AMZN

Brief analysis and latest updates here

OWL

Blue Owl Capital is an alternative asset management company, similar to Blackstone. Its focus is on direct originations of loans to private-equity backed and non-sponsored companies (middle-market and upper-middle-market companies). It has a net leases real estate platform. It also provides long-term minority equity and financing to private capital investment managers. A majority of the company's assets are funded by permanent capital, so it does not have withdrawal risk. Most of its earnings come from recurring fees from asset management without performance consideration, so the earnings stream is quite stable. Given it acquired STORE Capital (STOR) recently at a decent price, the management is very good.

Equity compensation related expenses were about 35% of DE that got added back into GAAP when getting DE. Its "true" EPS is about $0.1 per quarter, or about $0.4 in 2023. The P/E is about 30, not cheap, but not very expensive considering its growth is 15-20% annually. Another way to look at it is that its dividend yield is about 4.5%, and it's growing in double digits for at least 3+ years, which makes it quite attractive.

APO

Apollo specialized in distress situations, which reduced the number of competitors. Its famous slogan is purchase price matters, which shows how price conscious they are in picking investment. It has another slogan "we want 25% of everything and 100% of nothing on the asset", which is a goal post of the company about engaging in a lot of asset managing transactions even for other asset managers. It's a good way to position the company to have a large adjustable market. Their use of reinsurance company, Athene, helps them to grow assets under management effortlessly as well.

Expected 2023 EPS is $6.61, so P/E around 12, pretty cheap with an expected growth of 10-15%. 2.5% dividend yield helps a bit as well.

BN

Brief analysis and latest updates here

BAM

The pure asset management company part of the Brookfield Corporation. With BN, BAM can grow its asset under management (AUM) easily. Oaktree Capital, founded by the famous Howard Marks, is part of it, so it's very reputable.

The management has already indicated they are locked in to grow its cash flow 15% annually for the next field years. Its management fees do not rely on performance that much, so they are stable. With an expected 2023 EPS of $1.39, P/E 25 is not cheap, but with the help of 3.8% dividend yield (close to 100% payout, thanks to the asset light business model), there is a fair chance the stock can return 15% annually.

BX

A very reputable company in real estate. Its management fees rely on performance much more than Brookfield, but Blackstone has a track record, so I am not too worried about it.

Expected 2023 EPS is $4.36, P/E ~ 21. A 3.5% dividend yield with expected annual growth of 10-15%, this stock can potentially get a 15+% return in the long run.

CKHUY

CK Hutchison Holdings (OTC: CKHUY, SEHK: 0001) is a diversified conglomerate with interests mostly in telecommunications, retail, ports, infrastructure, and energy. The company was founded in 1979 by Li Ka-shing, one of Asia's richest men.

CK Hutchison is a well-managed business with a long history of profitability. The company has a strong track record of generating free cash flow, which it has used to invest in growth mostly by M&A, and return to shareholders through dividends and share repurchases.

CK Hutchison's businesses are all essential services that are not easily disrupted by new technologies or competition. This gives the company a moat that protects its profits and allows it to generate stable cash flow over the long term.

It is trading at $6/$18 ~ 33% of book value, P/E ~ 8, and a dividend yield of over 6%. The ADR costs probably $0.05-$0.1, which unfortunately is quite costly for lowly-priced stock like CKHUY.

HASI

Brief analysis and latest updates here

AHH

Brief analysis and latest updates here

EPRT

Brief analysis and latest updates here

MAIN

Brief analysis and latest updates here

BABA

Brief analysis and latest updates here

PAX

Brief analysis and latest updates here

GTY

Brief analysis and latest updates here

BNL

Brief analysis and latest updates here

WPC

Brief analysis and latest updates here

BIDU

Brief analysis and latest updates here

NVDA

Brief analysis and latest updates here

TSM

Brief analysis and latest updates here

SPY, VWO, MCHI

ETF Brief Descriptions and Updates

No comments:

Post a Comment